I bet you thought I was talking about Europe's sovereign debt issue but no, I'm talking about the average trade size for equities trading across Europe having just received some fascinating data from the Federation

of European Securities Exchanges (FESE).

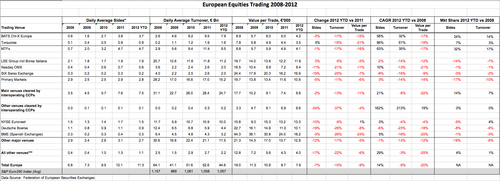

The data shows a considerable change in the

European equities markets over the past four years.

What the figures show is that the value per trade has been shrinking massively, thanks to high frequency trading and market volatility.

In 2008, the average daily trade on all European exchanges

was for €19,000. Today, it’s just €7,900

per trade, and decreasing at a CAGR of 20%.

Even more interesting is the impact of the Multilateral

Trading Facilities (MTFs), with BATS Chi-X trashing the market rising from an

average daily turnover of €2.6 billion per day in 2008 to €7.9 billion today

(it was €9.5 billion daily last year).

Turquoise has also seen an increase, from €200 million a

day in 2008 to €1.6 billion a day today (€1.9 billion last year).

Who’s the loser?

LSE Group, NASDAQ and SIX Swiss Exchange who have seen

their daily turnover halve from a combined €28.2 billion per day in 2008 to

just €15.2 billion today.

If you’re into this stuff, here’s the spreadsheet

Download FESE numbers (thanks to Diana Chan at EuroCCP for sending over).

If you cannot download, double-click and zoom on the image below:

Equally, if you’re into this stuff, you may want to come

to the next Clearing & Settlement Working Group plenary meeting on 11th

December at the offices of Kemp Little, 138 Cheapside (near St Paul’s).

The agenda is currently being firmed up, but will

include:

- The Risk, Regulation, Infrastructures and

Technology Subject Groups updating on progress to date; - A special keynote from Mark Davies Vice

President, Data Business Development, DTCC, who will cover the LEI story to

date, DTCC's CICI utility, FSB progress and the next steps on global LEI

programme; - Details of the CAS-WG’s special and new partnership

with the A-Team;

and a few other surprises.

Attendance is free so come along (just register here).

Chris M Skinner

Chris Skinner is best known as an independent commentator on the financial markets through his blog, TheFinanser.com, as author of the bestselling book Digital Bank, and Chair of the European networking forum the Financial Services Club. He has been voted one of the most influential people in banking by The Financial Brand (as well as one of the best blogs), a FinTech Titan (Next Bank), one of the Fintech Leaders you need to follow (City AM, Deluxe and Jax Finance), as well as one of the Top 40 most influential people in financial technology by the Wall Street Journal's Financial News. To learn more click here...