I was at a conference yesterday where a leading economist

talked about the global economic forecasts and specifically about the UK.

When he got to the UK, he started talking about which sectors

were expanding and succeeding the most, citing the telecommunication, transport

and logistics areas as those with the greatest opportunity.

In other words, people doing business on the internet and

ordering stuff for delivery to the home or office.

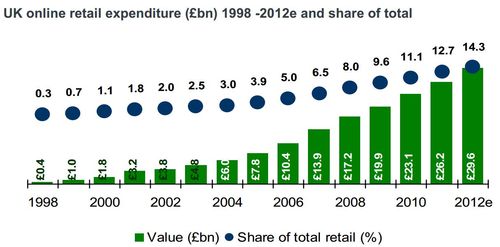

It certainly seems to be true when you look at the

stats. For example, the online retail

markets are growing rapidly, with 12%+ growth forecast for the next year (double-click

chart for larger image).

Source: Verdict Research

But this belies another story, which is that internet

retailing is now maturing, as year-on-year growth accelerates at a decelerating

rate .

Source: Verdict Research

And, as the internet matures, the old retail space withers

and dies.

This has been illustrated well by the demise of our

oldest music retailer (HMV), camera retailer (Jessops), electronics retailer (Comet) and entertainment retailer (Blockbuster) …

All of these bankruptcies were announced in just the past month. Meanwhile, Amazon and iTunes march onwards and upwards.

This change in high street to home has been inevitable and

obvious for years, with many predicting the demise of anything that can be

electronified.

This is why travel agents, book shops and more have

disappeared en masse for the past decade in most economies (just look at

Borders and Tower Records).

That’s why my High Street stores are empty, shut down,

closing, dead …

It just makes me wonder why the leaders of these retailers didn't get it earlier and switch their business models from high street to home, from instore to online?

They must have been mad.

And if you accept everything I’ve written above, then why

the hell are retail banks still operating and even expanding their retail store footprint?

Source: This is money

Chris M Skinner

Chris Skinner is best known as an independent commentator on the financial markets through his blog, TheFinanser.com, as author of the bestselling book Digital Bank, and Chair of the European networking forum the Financial Services Club. He has been voted one of the most influential people in banking by The Financial Brand (as well as one of the best blogs), a FinTech Titan (Next Bank), one of the Fintech Leaders you need to follow (City AM, Deluxe and Jax Finance), as well as one of the Top 40 most influential people in financial technology by the Wall Street Journal's Financial News. To learn more click here...