I finally got around to taking a good look at the Square

cash announcement today.

If you didn’t spot it, Square announced last week that you

can send cash to anyone via email for free.

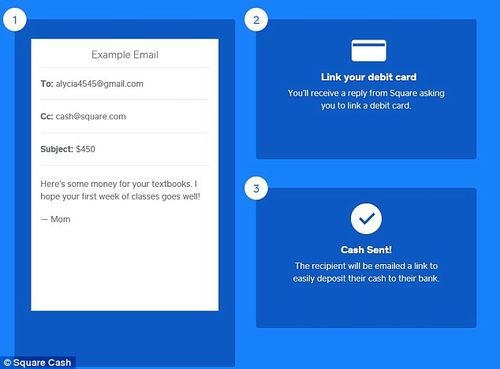

All you need is to provide your debit card details and then you send an

email to the payee with the subject line stating the amount and cc cash@square.com. When the payee receives the email, they enter

their debit card details and the money is moved.

That’s all there is to it.

It takes seconds and it’s done.

You can send up to $2,500 a month to friends via Square Cash

or $250 a week to any email address. Once

signed up, you just need to put cash@square.com

on the emails thereafter and away they go. And your money too.

You can also link apps on Android and iPhone to get alerts

when cash is sent and received too.

And the best bit is it’s free.

This last bit is the most startling piece for me, as Square

is not charging any fees for the transaction.

How does it make money?

I guess, like Twitter and Facebook and Google, it starts with

the idea and , over time, funds itself through ads.

So you send your cash and your friend gets an ad saying, “spend

that $250 you just received on a new phone”.

Right now, Square Cash is purely for US currency debit cards

(when will they open overseas?), and there’s one big question that Quartz raises.

Can you trust Square Cash?

They spotted that Square clearly articulates that it will

not be liable for any fraudulent transactions, even though they assure Quartz

that they are safe and use algorithms to ensure fraud does not occur.

The thing is that, if it did occur, Square provides no

reimbursement or guarantee.

It is this last bit that intrigues me about human behaviour,

as banks believe they are trusted because they provide a guarantee.

If you lose money, you get ti back.

In the UK, you get up to £85,000 back*.

So let’s play this out.

You start using Square, you start to trust it, so you start

to transfer more and more money through it.

Then you lost $2,000 and have no compensation or recompense.

Is that fair?

What about Google Gmail or other services? Do you trust them even though there is no

deposit guarantee or cover?

Over time, that’s the reason why Square and Google will join

some form of guarantee scheme.

In the meantime, Square Cash is a great innovation. You just need to be a wee bit careful with

how you use it.

Take note from the Square Wallet User Agreement:

15. Security.

We have implemented

technical and organizational measures designed to secure your personal

information from accidental loss and from unauthorized access, use, alteration

or disclosure. However, we cannot guarantee that unauthorized third parties

will never be able to defeat those measures or use your personal information

for improper purposes. You acknowledge that you provide your personal

information at your own risk.

* Most people think this guarantee is £100,000 in the UK

btw, but it’s €100,000 not £100,000.

Hence it was translated into UK cover as £85,000.

Chris M Skinner

Chris Skinner is best known as an independent commentator on the financial markets through his blog, TheFinanser.com, as author of the bestselling book Digital Bank, and Chair of the European networking forum the Financial Services Club. He has been voted one of the most influential people in banking by The Financial Brand (as well as one of the best blogs), a FinTech Titan (Next Bank), one of the Fintech Leaders you need to follow (City AM, Deluxe and Jax Finance), as well as one of the Top 40 most influential people in financial technology by the Wall Street Journal's Financial News. To learn more click here...