Just got a note from SWIFT today about a new publication they’ve commissioned with BCG (Boston Consulting Group) into World Payments.

Seems a bit strange as McKinsey and CapGemini already product great reports in this space.

I don’t mind having another one though, especially as the results have been verified by the SWIFT network, so all numbers are deemed to be pretty accurate here.

Here’s the summary:

In the years following the 2008-2009 financial crisis, the payments and transaction banking businesses have been vital revenue generators for banks.

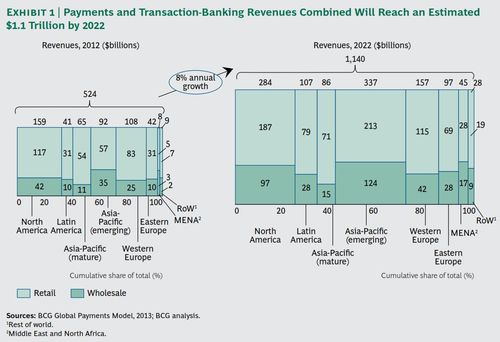

In 2012, these businesses generated $301 billion in transaction specific revenues (including monthly and annual card fees) as well as $223 billion in account related revenues (including account maintenance fees and spread revenues).

The total represented roughly one-quarter of overall global banking revenues. Banks handled $377 trillion in non-cash transactions in 2012, more than five times the amount of global GDP.

And business keeps growing steadily. By 2022, payments and transaction banking revenues will reach an estimated $1.1 trillion, a compound annual growth rate (CAGR) of 8 percent.

The revenue mix is expected to shift toward account-related revenues as yield curves steepen and as pressure on transaction fees persists. The value of non-cash transactions will reach an estimated $712 trillion by 2022, a CAGR of nearly 7 percent.

Overall, payments related businesses have continued to service as a relatively stable source of income for banks, providing a solid platform on which to build customer loyalty and increase share of wallet. Moreover, with the exception of credit cards, payments businesses still possess structural advantages as consistent, predictable volumes and relatively low (non-capital intensive) risk factors. These businesses have helped banks considerably by providing a low-cost source of funding and liquidity.

At the same time, payments related businesses continue to face challenges on multiple fronts. Regulatory pressures stemming not only from the implementation of the Single Euro Payments Area (SEPA), but also from interchange fee legislation, along with intensifying competition and disruption by new entrant, are taking a toll.

In addition, the attributes of payments businesses have attracted non-bank providers in key areas such as mobile payments and related deals and offerings on the retail side, and in supply chain financing on the wholesale side. The cumulative impact of these forces is evident. The average per-transaction fees earned by banks are broadly poised to decline, particularly in mature markets.

Given the size of the revenue pools at stake, banks will have to adapt to this “new new normal” climate and sharpen their business and operating models accordingly. Particularly in mature markets, higher levels of customer-centricity and a greater emphasis on execution excellence will be key success factors in winning share from competitors. Crisper pricing strategies, along with more efficient processes and systems, will become core capabilities for maintaining margins and, even more important, for cross-selling.

There’s a lot more, and you can find the full report here.

Chris M Skinner

Chris Skinner is best known as an independent commentator on the financial markets through his blog, TheFinanser.com, as author of the bestselling book Digital Bank, and Chair of the European networking forum the Financial Services Club. He has been voted one of the most influential people in banking by The Financial Brand (as well as one of the best blogs), a FinTech Titan (Next Bank), one of the Fintech Leaders you need to follow (City AM, Deluxe and Jax Finance), as well as one of the Top 40 most influential people in financial technology by the Wall Street Journal's Financial News. To learn more click here...