At the start of the year I made 14 predictions for 2013.

Here they are.

First, four forecasts for the economic movements of 2013.

1. The USA is a solid rock

From the Economist

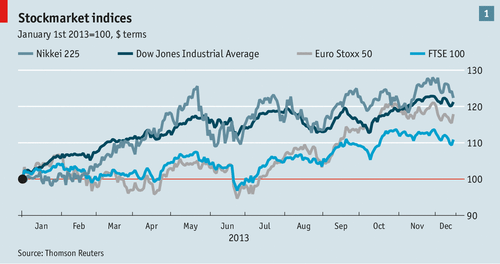

I thought the US would be stable this year, but with the stand-off between the Democrats and the Republicans reaching a fiscal cliff, this was not the case. The dollar has been stable, so you could say that this part is solid as a rock, but the economic performance has flat-lined and the underlying news is more disturbing.

From Business Insider:

Many on Wall Street believe the American economy will finally pick up in 2014. BofA Merrill Lynch chief investment strategist Michael Hartnett argues "escape velocity" is "tantalizingly close." Nonetheless, it hasn't happened yet, and the ultimate debate about the future of the U.S. economy is still this: can it?

And from Harvard Business Review’s blog by Umair Haque:

The economy is indeed “growing.” But the top 1 percent have taken 95 percent of the gains in this so-called “recovery.” The plain fact is that the average household is poorer in the “recovery” than during the “recession.” We cannot suggest that an economy is perfectly fine—nay, even healthy—just because a tiny number are growing richer while the lives of the vast majority are literally growing shorter, nastier, dumber, harder, and bleaker.

2. South America is the place to be

From the Economist

Yes. Southern America’s growth rates are impressive compared to Europe, but its growth is slowing. From the Guardian:

Largely as a result of sluggish global demand, particularly from China – now the biggest trade partner of many countries in the region – Latin America's economic growth slowed to less than 3%. This was the lowest level in five years, but a stellar performance compared to the eurozone, further underscoring the shift in wealth from the old to the new world. Speeds varied enormously from country to country. Paraguay, Panama and Bolivia led the pack; Chile, Peru, Argentina and Ecuador maintained a steady clip; the two major economies – Brazil and Mexico – were sluggish; and Venezuela came close to slipping into reverse. So far, however, in most countries, employment remains stable and benefits to poorer communities are at or near historic highs.

3. China becomes a hot consumer market

From the Economist

Chinese consumers spend more online than American consumers (there are more of them too) and their key consumptions trends can be easily understood if you research a bit. For example, WPP summarise the top 10 trends as:

- Pay for Safety

- Go Micro

- Culture Consumption

- Spending on the Young

- Spectacular Singles

- Charity is the New Fashion

- Emotional Consumption

- Gray Hair Craze

- Super 3rd Party

- Crossover Economy

China may be becoming a hot consumer market, but its inequality is a key challenge.

China is rapidly becoming a highly unequal country, politically, economically and socially. Intergenerational transmission of inequality and the emergence of class solidification within a short period of time have institutionalized the root causes of inequality. China’s strategic goal of avoiding the middle-income trap is therefore fundamentally contingent upon how it will address the inequality crisis. Managing this challenge will require a comprehensive reassessment of the future trends, institutional roots and consequences of current inequality.

4. The Eurozone stays together with fissures, cracks and holes

Strangely enough, the Eurozone was pretty quiet in 2013. Thank goodness for that! And yes, it is still together with no country leaving and Croatia joining, with others to follow.

Mind you, it is not a good news story. In fact, Europe remains pretty depressed. From the Guardian:

To listen to the sermons from top people in Brussels and in some European Union capitals, the euro is safe, the storm has been weathered, the existential questions about the viability of the single currency have been banished. Good job.

But four years after Greece went hypercritical, triggering a eurozone sovereign debt crisis and a reshaping of how the EU works, the social, economic and political costs of the upheaval are coming home to roost. There are no quick fixes.

Austerity, the main policy response, has been savage. It is taking its toll. The eurozone is mired in stagnation, on the brink of deflation, gross domestic product remains 3% below 2008 Lehman Brothers levels. Growth is so anaemic, low fractions of a decimal point, that at current levels it will take the eurozone until 2021 to return to 2008 GDP levels.

In the words of a recent study from the International Institute for Strategic Studies, the eurozone faces a lost decade. Youth unemployment rates are catastrophic, more than 50% in Greece, Spain and Croatia, commonly around 25% around large swaths of Europe. And if there is recovery to speak of, it looks like jobless recovery

All in all, the 2013 hindsight is one that leaves the world looking pretty challenging from an economic view. Having said that, Africa looks very promising.

Bob Diamond, ousted as boss of Barclays last year after the Libor-rigging scandal, potentially stands to reap millions of pounds from a new stock market venture set up to acquire financial services companies in Africa.

Then I made five banking predictions:

1. A major bank (not Goldman Sachs) will show they are doing God’s Work

I reckoned that a bank like Barclays would get back to basics, shut down key operations that were not in the customer’s interests, and leave markets where they historically made money. They have taken some of these actions but, more interestingly, the talk of 2013 has been about big banks being too big to manage and a call for the breakup of the big banks.

JP Morgan is one the reasons for the discussion, especially after the London Whale issue.

JPMorgan is the result of relentless M&A. It houses the former Chemical Bank, Manufacturers Hanover Trust, Chase Manhattan, First Chicago, Banc One, and Morgan Guarantee Trust – to name but a few. Since the crisis, Bear Stearns and Washington Mutual have joined the fold. Each component was a large and complex institution. Many ranked within the top 10 of their day. So not surprisingly, JPMorgan is a veritable banking behemoth.

Its balance sheet weighs in at more than $2tn according to its US accounts; $4tn if European rules, which do not allow exposures to derivatives to be netted off, applied. As global agreements for the resolution of global banks are not yet in place, JPM remains both too big and too interconnected to let fail. Yet given that bank’s slender sliver of loss-absorbing capital, it might also prove “too big to bail”.

So regulators, and the public purse they protect, must ask: “Is the bank sufficiently well managed? Can it ever be?”

When the supposedly best run bank in the world shows that it cannot manage itself, can any bank?

Apparently not according to John Reed, the former CEO of Citibank that lobbied for the repeal of Glass-Steagall fifteen years ago.

If anyone is qualified to judge the success of combining investment and commercial banks in the same institution, it is John Reed. As chief executive of Citicorp in the 1980s and 1990s, he evangelised the attempt to create a “one-stop shop” selling many different products and took the bank into its historic merger with Travelers Group to form Citigroup in 1998.

That deal redefined banking in the US and triggered a repeal of the old Glass-Steagall split between investment and commercial banking in the US, which some critics have blamed for being the root cause of the 2008 financial crisis.

But now a group of politicians in the US is attempting to reintroduce the split, arguing that Glass-Steagall’s repeal contributed to the financial disaster that took place a decade later. Citigroup itself needed several injections of capital from the US government in the fraught months following the Lehman bankruptcy.

Now retired, Mr Reed firmly believes that the business logic behind the transaction was flawed, and that the old Glass-Steagall division should be reinstated.

Back to basics banking was the mantra of 2013, and this will continue in 2014.

2. A Chinese bank will make a play in the USA

Not really

3. Many banks will announce radical mobile offers

Yes, this one was a safe bet with many banks getting into mobile big time. My favourite announcement has to be Banco Sabadell’s Google Glass app though.

4. Another bank will be severely embarrassed by their technology

Well, one bank was severely embarrassed by another technology failure. The same one as last year: RBS. However, they were not the only one:

- #BARCLAYSGLITCH – BRANDED BANK OUTAGES?

- Chase Bank site attacked, suffers intermittent outage

- Bank of America Plagued by Online, Mobile Outages

- China bank outages trigger consumer cash worries

- Westpac suffers online banking outage

and there were more. A sure sign of legacy systems requiring or being upgraded.

5. RBS and Lloyds will become stable bets for the future

Maybe just Lloyds right now, taking note of #4.

And the five key technology trends of 2013 I focused upon were:

- Big Data Analytics

- Cloud

- Mobile

- The Internet of Things

- 3D Printing

All of which have become notable in 2013, along with the trend to wearable (which some would say is the internet of tings).

Anyways, I’ve run out of time to elaborate further, but would give these predictions a 85% accuracy rating, which isn’t bad when predicting the (near) future.

2014 predictions to come in January.

Chris M Skinner

Chris Skinner is best known as an independent commentator on the financial markets through his blog, TheFinanser.com, as author of the bestselling book Digital Bank, and Chair of the European networking forum the Financial Services Club. He has been voted one of the most influential people in banking by The Financial Brand (as well as one of the best blogs), a FinTech Titan (Next Bank), one of the Fintech Leaders you need to follow (City AM, Deluxe and Jax Finance), as well as one of the Top 40 most influential people in financial technology by the Wall Street Journal's Financial News. To learn more click here...