I introduced the business model debate about banks yesterday, as the discussion always comes back to the new competition. Who are the new competition? Are they the upstart fintech startups or are they Google, Amazon and brethren?

The answer is it’s both, but I wouldn’t worry about Google, Amazon and co as much, as they are attacking banks in a very different space to the way in which the fintech startups are. The startups are attacking narrow finance and trying to replace core bank functions like credit and payments with new capabilities. The TransferWise and Lending Club business models should worry banks. But the others? I’m not so sure.

Yes, they’re big and cool but what is their space?

Processing.

It was when I was talking about the quote that everyone uses now from Techcrunch …

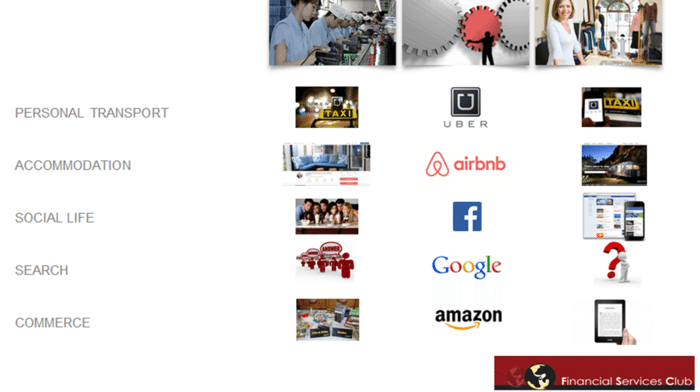

Uber, the world’s largest taxi company, owns no vehicles. Facebook, the world’s most popular media owner, creates no content. Alibaba, the most valuable retailer, has no inventory. And Airbnb, the world’s largest accommodation provider, owns no real estate. Something interesting is happening.

… that I realised yes, something very interesting is happening. It’s called infomediation, and we’ve seen it coming for years. We just wonder why we aren’t doing it ourselves for.

If you take my business model chart, the Uber’s, Facebook’s and Alibaba’s are all operationally excellent processing houses. They have no product or service themselves and, if you think about it, they have no customer relationship either. They just have a great ability to connect those who need with those who have in real-time.

- I need to get from A to B – connect me with someone who has a car to drive me.

- I need to stay overnight in this place – connect me with someone who has a spare bedroom to sleep in.

- I need to share my social life – connect me with all my friends and family who might be interested in it.

The same with Amazon and Google.

- I need to buy some stuff – connect me with the lowest cost provider and get it delivered.

- I need to find some stuff – connect with the information I need.

In other words, all of these great new companies are infomediating the content – cars, beds, photos and updates, products, information – with the context – the app in my hand or the page that I’m browsing from the place where I’m at. Their processing is recognising our context and delivering the content.

If I therefore drew my chart for the new world of infomediation that we admire (the Ubers, Airbnbs, Facebooks, Amazons and Googles) it would look like this:

And then I come to the question: what is the processing machine for banking and what is the role of banks around that machine?

It’s a great question as, historically, the processing engine for the financial system has been SWIFT, VISA, MasterCard, TARGET2, STEP2, FedWire, CHIPS, BACS and more. Now this is not going to disappear fast, if at all, but there is a new marketplace structure appearing. Originally, I would have said it was PayPal, as they’ve removed the friction of paying digitally, but it’s not PayPal. PayPal are good but … they haven’t changed anything.

Then it came to me. The reason why we’re so excited about the internet of value is that the blockchain is our new processing engine.

The blockchain can infomediate the financial system to deliver our processing engine for value exchange: I want to exchange value – connect me with the right value tokens and value stores to exchange.

The thing is that the blockchain is not the engine. It’s the technology. So right now, there’s an open ground for something, someone or some firm to own that space. Watch the ensuing debate as Ripple, Eris and Ethereum and more fight for that space.

Chris M Skinner

Chris Skinner is best known as an independent commentator on the financial markets through his blog, TheFinanser.com, as author of the bestselling book Digital Bank, and Chair of the European networking forum the Financial Services Club. He has been voted one of the most influential people in banking by The Financial Brand (as well as one of the best blogs), a FinTech Titan (Next Bank), one of the Fintech Leaders you need to follow (City AM, Deluxe and Jax Finance), as well as one of the Top 40 most influential people in financial technology by the Wall Street Journal's Financial News. To learn more click here...