One of the gating factors to financial inclusion is the mobile network itself. It sounds simple to say that all of Africa can have access to mobile money, and they can, but if each telco has different wallet structures, charges and fees, then the ease of usage falls sharply. This is why interoperability is a key factor and Tanzania leads the way in this regard.

In February this year, the three leading MNOs – Vodacom, Millicom’s Tigo and Airtel – announced full interoperability. Vodacom’s participation means that over 16 million mobile money users in Tanzania will be able to send payments to each other, regardless of which mobile operator they use. That is a key achievement, with the country claiming to be the first in Africa with full interoperability.

Will others follow? It remains to be seen.

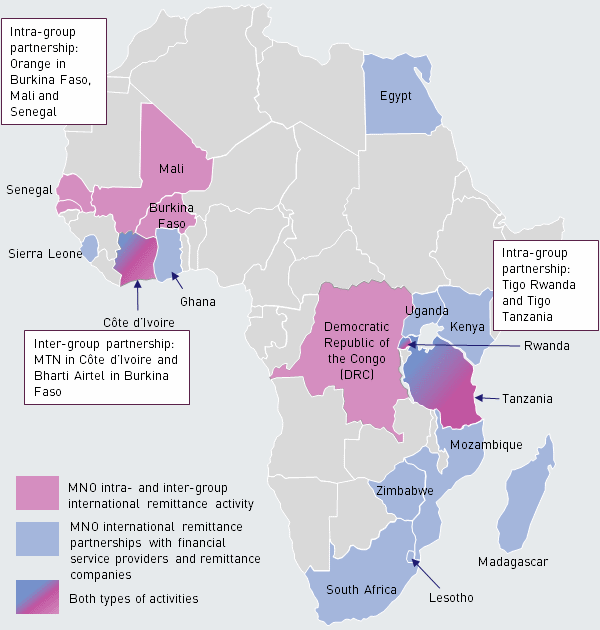

Right now it’s a challenge with some countries actively encouraging inter- and intra- operator partnerships and agreements to enable domestic and cross-border mobile money transfers cheaply and easily ...

Chart from Analysys Mason

...whilst others prohibit such activity, such as Nigeria. This is why, according to the World Bank, Sub-Saharan Africa mobile financial inclusion varies immensely:

Percentage of population using a mobile money account, 2015

Sub-Saharan Africa average 11.5%

Ghana 13.0%

Kenya 58.4%

Nigeria 2.3%

South Africa 14.4%

Tanzania 32.4%

Uganda 35.1%

Zimbabwe 21.6%

As can be seen, it varies widely and is a reflection of the regulatory structure and enthusiasm to adopt mobile wallets amongst the banks and MNOs. For example, in Tanzania, 25 banks are involved with the MNOs to allow mobile financial inclusion. The process has been supported by the Bill & Melinda Gates Foundation and has resulted in over half of Tanzania’s GDP moving through mobile wallets each month.

Compare that with Nigeria where 45% of the population have a mobile subscription and yet only 2.3% are using mobile money. Why?

Because not every country is the same. Just because mobile money can succeed in Kenya, Tanzania and Uganda does not naturally mean it will succeed in Nigeria. Nigeria has a large unbanked population who aren’t aware of mobile money for example. Even though the Central Bank of Nigeria has introduced measures to encourage mobile financial inclusion, the introduction of mobile money in Nigeria has been bank-led, rather than MNO-led, and the banks have not done a great job of advertising the capability. For example, a survey by Philip Consulting last year found that over a third of Nigerians weren’t aware you could make payments by mobile and, of those who did, the trust in the network is low as Nigeria is first and foremost a cash-based economy. This is why many will not use electronic transactions but prefer to use informal financial providers called esusu, adashe and ajo.

As can be seen, Africa is not a big homogeneous land mass of all citizens using mobile money, but it is one where mobile money is taking off rapidly. In 2015, 82% of Africans have a mobile phone and, of those who do, 1 in 3 have a mobile wallet. These numbers are also rising rapidly and resulting in new competitive structures.

For example, seeing the success of M-Pesa led to Equity Bank in Kenya launching their own mobile network service Equitel, in partnership with Airtel, and offering better rates on payments, savings and transfers. This resulted in the operator of M-Pesa, Safaricom, launching a legal battle which they lost and then trying to block Equitel by charging high costs for transfer outside the M-Pesa network.

This is interesting as Safaricom were attacked by the banks during their start-up years for fear of fraud and fee losses. These fears were unjustified and resulted in the turnaround of the banks from fighting against M-Pesa to working with them to competing with it. Meanwhile, M-Pesa moved from offering basic mobile money transfers to full paperless banking services through M-Shwari.

It is fascinating to watch these changes in Africa, based upon mobile enabling all to use the network. It is not just based upon mobile network services however. More on this tomorrow. Meanwhile, just to wrap up, here’s a summary of mobile financial inclusion from Safaricom Vodafone.

Financial inclusion

Our M-Pesa mobile money transfer service offers people without a bank account access to financial services through their mobile phone, enhancing their ability to improve their lives and livelihoods.

M-Pesa was launched in 2007, enabling people to transfer small amounts of money to friends and family safely and affordably via their mobile phone. It is now a well-established part of our business with over 19.9 million active users1 in nine markets.

M-Pesa continues to evolve beyond traditional money transfer services, enabling people to save and borrow money, receive salaries and benefits, pay for goods and services and more. It also supports solutions that can improve lives and livelihoods in other areas such as Agriculture and Health.

Extending access to finance

M-Pesa is helping to extend access to financial services, particularly in markets where a high percentage of the population are ’unbanked’ – people who do not have access to a bank account.

Now well established in both Kenya and Tanzania, M-Pesa continues to have a strong and growing presence in Africa. Since 2013, it has been extended to the Democratic Republic of Congo, Egypt, Lesotho, Mozambique and South Africa.

In 2014/15, we completed our national rollout of M-Pesa in India, where 60% of adults are unbanked. We collaborated with ICICI Bank to support domestic money transfers that help migrant workers send money home to their families in a safe, secure and inexpensive way. This was also the first full year that M-Pesa has been available in Romania – its first European market – where 39% of the population do not have bank accounts2. The service offers access to mobile money transfer and payment services to approximately 7 million Romanians who rely mainly on cash transactions.

There are now 19.9 million active users of M-Pesa worldwide. In 2014/15, the number of active users increased by 18% and we processed 3.4 billion transactions, up 20% from 2013/14.

Investing in distribution agents and outlets is critical to the success and accessibility of M-Pesa. We have approximately 273,000 agents across all M-Pesa markets, extending access to mobile financial services as well as offering employment opportunities.

We are also investing in ambassador programmes to help new customers feel confident and comfortable using the service. In 2014/15, our ambassador programme in Tanzania helped to increase the number of women in our distribution network. So far, approximately 1,400 women have completed their training.

Developing new mobile money solutions

We are extending M-Pesa services beyond basic money transfers to enable people to save and borrow money, send and receive money internationally, make cash-free payments for goods and services, and receive salaries and government benefits securely, regardless of whether they have a bank account.

In a collaboration between Vodacom and the Commercial Bank of Africa, M-Pesa customers in Tanzania can now access interest-bearing savings accounts through a mobile money service known as M-Pawa. M-Pawa customers can take out small loans and earn interest on savings as small as one Tanzanian shilling (equivalent to around a thirtieth of a penny in the UK).

This builds on a similar product launched in 2013/14 in Kenya, known as M-Shwari, which now has 5.8 million active customers. In 2014/15, M-Shwari customers gained access to a new mobile savings plan, Lock Savings Account, which enables them to save money through a fixed deposit and earn higher rates of interest.

Merchants in Kenya and Tanzania can now accept payments for goods and services from their customers via their mobile phones using the M-Pesa Buy Goods functionality. The ability to receive payments through this service, known as Lipa Na M-Pesa in Kenya and Lip Kwa M-Pesa in Tanzania, makes business owners less susceptible to the risks of handling cash, such as theft and fake currency. People in Kenya can now also use M-Pesa to top up cashless travel cards for public transport.

Our M-Pesa International Money Transfer service continues to expand. People can now use the service to send and receive money directly from their M-Pesa accounts between Kenya and Tanzania. In addition, funds can be sent to M-Pesa accounts from a growing number of countries through our international remittance partners, such as MoneyGram and WorldRemit. Increasing mobile money transfers into developing economies supports economic and social development. It provides more choice for senders of cross-border money transfers and gives M-Pesa customers a cheaper, more convenient way to receive money.

Vodafone partnered with the National Rural Health Mission and Rural Employment Guarantee in 2014/15, to use M-Pesa to disburse much-needed government benefits in the states of Bihar and Jharkhand in India. In recognition of this work, M-Pesa was named ’most inclusive digital wallet’ and received the Financial Inclusion through Business Innovation Award at the 2015 BFSI Leadership Awards in Mumbai.

Notes:

- Active users are those who have made a potentially chargeable transaction in the last 30 days.

- World Bank, 2014

Chris M Skinner

Chris Skinner is best known as an independent commentator on the financial markets through his blog, TheFinanser.com, as author of the bestselling book Digital Bank, and Chair of the European networking forum the Financial Services Club. He has been voted one of the most influential people in banking by The Financial Brand (as well as one of the best blogs), a FinTech Titan (Next Bank), one of the Fintech Leaders you need to follow (City AM, Deluxe and Jax Finance), as well as one of the Top 40 most influential people in financial technology by the Wall Street Journal's Financial News. To learn more click here...