I wrote a blog the other day for The Next Web. I thought it was ok, and it has gained a lot of traction socially. Apparently, people like it and here I’m going to expand upon the basic theme to give a detailed analysis of how FinTech wings are spreading.

There’s been a lot of talk about fintech lately. We talk about the billions of dollars being invested in fintech; the wave of unicorns and start-ups in this space; the challenge they bring to banks and incumbents; the way in which they are reaching new spaces and places; but what is fintech? It is no longer this big bucket of finance and technology. In fact, saying ‘fintech’ is like saying ‘retailer.’ But what exactly are they retailing and, in the fintech sense, what areas of finance are these companies automating?

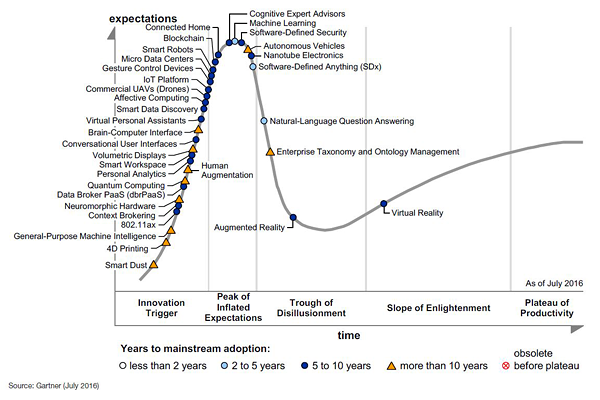

This gets interesting as we now have a market that is spreading its wings into lots of different areas. It is no longer one big bucket, but many. There is RegTech for Regulatory Technologies; WealthTech for Wealth Management Technologies; InsurTech for Insurance Technologies; and so on. Then FinTech has also gained subcategories like Lending, Analytics, Digital Identity, Cybersecurity, SME Finance, Financial Inclusion, Payments, Roboadvice, Blockchain Distributed Ledgers, Neobanking and more. Then there are also some generic technologies around Cloud, the Internet of Things, Artificial Intelligence, Machine Learning, Biometrics and others that are also creating FinTech themes and impacts. Well, this blog will look at the range of services we are discussing here, and map them onto the Chris Skinner FinTech Wave (loosely based on Gartner’s Hype Cycle).

Because there are so many categories, I’m not going to get through them all in one go, so guess I need to split this into two blogs.

So, here is the FinTech Wave, Part One.

RegTech

Regulatory Technologies, or RegTech for short, is fairly obvious as to what it is. Just in case it’s not obvious though, I would define it as technologies that help banks comply with regulatory requirements more easily and at a lower cost or that help regulators monitor bank activities more accurately in real-time. I’m not going to do a big write up here, as I’ve blogged a lot about RegTech, so you can read the blogs on this:

- RegTech: Brother in Arms with FinTech

- Regulations, Innovations, Sandboxes and #RegTech

- Real-time connections between regulators and banks is a game-changer

- The Semantic Regulator (#RegTech Rules)

- The Catch 22 of Banking

- The Bank of England: taking the lead in #FinTech

- The Monetary Authority of Singapore: keeping up with the Bank

- America’s regulatory issue is too many cooks

InsurTech

Insurance Technologies, InsurTech, are rethinking and redefining how we deal with insurance through technology. As with RegTech, I’ve blogged a bit about this, so you can read on over here:

If you can’t be bothered, then here’s a list of interesting InsurTech start-ups:

Augury makes sensors for heating, ventilation and air conditioning systems

BimaAfya is connecting low income populations in sub-Saharan Africa with health insurance

Buzzmove provides price comparison for the removals trade; information that is important to insurers after a loss

Cocoon makes an internet-connected security device for the home

CoVi Analytics is a platform for insurers to use the required reporting from Solvency II data in their enterprise in other ways

Domotz is an Internet of Things management system that offers a platform for insurers to rate risk and manage claims

FitSense helps life and health insurers leverage data from wearables

Friendsurance, the world’s first peer-to-peer insurance firm

Kasko provides a white-label option for instant insurance purchases on affiliate platforms.

Lemonade is a US-based peer-to-peer insurance firm that offers fast and low cost homeowners insurance, powered by technology, that mixes the Friendsurance and Trov models

MassUp uses APIs to connect insurers to retailers so people can quickly and easily add coverage to new purchases.

Myfuturenow helps connect dormant pension accounts to holders.

Quantifyle allows users to “shop around” their wearable and other health data to insurance companies and find the best price

Rightindem is a self-service total loss claims platform that claims to reduce insurers workload and leakage while improving customer service

Roost makes a smart battery for smoke detectors and counts USAA among its investors

Safer is designed to help millenials identify what kind of insurance they need by tapping into their social data

Trov where you pay-as-you-need insurance

WealthTech

I haven’t blogged about WealthTech much, because it’s just rising. Although the term is used reasonably liberally towards the end of 2016 online, most of what I see being written about it is related to roboadvisory services. That’s not right as roboadvice is for the masses, not the High Net Worth or Ultra-Wealthy, with is what WealthTech relates to, not the mass affluent. That is why I’ve kept Roboadvice as a separate categorisation to WealthTech.

Susanne Chishti is working on a WealthTech book, and wrote recently over at Silicon Republic the following analysis:

Wealth and asset management firms have to review their internal processes and communication with clients and decide where tools provided by the fintech industry can be applied to enhance their proposition and operations. These can be client-facing tools (for example, providing more accessible information in digital formats), portfolio management tools that enhance performance, or tools providing the relationship manager with powerful solutions so that she can serve her clients more effectively …

The future success of asset and wealth management firms in our evolving digitised world will depend on their ability to leverage fintech innovations to achieve better performance at lower costs combined with better customer service.

It is safest not to underestimate the seismic shift fintech will have on the global asset management industry. This sector has the opportunity now to challenge its own structures, business and revenue models to reinvent itself, fight complacency and act now to accelerate the internal pace of innovation and collaboration with the fintech ecosystem.

Meanwhile, Susanne picks out 11 firms worth watching in the WealthTech space:

AlgoDynamix: an innovative risk analytics company that detects disruptive events in global financial markets and anticipates price movements, thus providing advance warning to asset managers to improve higher risk-adjusted returns.

Delio: an investment platform that better connects a financial institution’s high net-worth clients with private market opportunities.

DriveWealth: a FINRA-registered broker-dealer that provides low-cost global retail access to the US equities market.

InvestGlass: a robo-advisory model that offers an automated selling tool fully customisable for retail and private bankers. Its artificial intelligence-based solution helps professionals generate the right investment case for the right client at the right time, compliant with MiFID II.

Investivity: empowering wealth managers by capturing the essence of the best funds at a fraction of their costs and allowing them to personalise for their clients’ needs.

KYC3: developing solutions using machine learning, big data and blockchain in order to transform regulatory and reputational KYC risk management.

Prophis: a tool that identifies those emerging developments that are most likely to have an impact on the performance of a particular portfolio and communicates them in a novel and visual way.

Quantesys: software that identifies and interprets behavioural anomalies to enhance investors’ profit and reduce their portfolio volatility.

Tradency: a pioneering financial technology provider, focusing on B2B product development of a full-stack digital investment and trading ecosystem.

Videodesk: a platform that reinvents how companies sell to and service their customers by enabling experts to have rich conversations around investment products with qualified prospects.

Walnut Algorithms: an advanced machine learning and applied mathematics for absolute return quantitative investment strategies.

Just to balance this with another view, there is an interesting take on WealthTech in Asia from FinTech News http://fintechnews.sg/7609/personalfinance/top-9-wealthtech-startups-singapore-hong-kong/ :

Mesitis is a financial technology company headquartered in Singapore focused on developing solutions for the private wealth market. The firm offers an account aggregation and reporting platform for high networth individuals and their wealth managers; a bionic investment advisor providing unconflicted, custom-built, ETF-only portfolios at a fraction of the cost; and an agency-only execution provider specializing in both global equity & fixed income markets.

8 Securities Limited is known for having launched Asia’s first zero commission mobile stock trading service. The app lets users trade 15,000 US, Hong Kong and China H shares and exchange traded funds for free. Users can hold their account in USD, HKD or RMB. There is no minimum balance or account fee.

Quantifeed provides a digital investment solution to financial institutions and their clients. The platform allows users to explore, customize, invest and manage portfolios of stocks, bonds, funds and other asset classes. It has been developed to allow for full integration with firms’ execution and back office systems.

MyHero is the company behind TradeHero, a popular free stock market simulation app, which draws real-world data from stock exchanges to create a global social investment network.

FinFabrik is a financial services technology company that focuses on investment-related services, ranging from active client trading to automated wealth management platforms.

Prive Financial provides a comprehensive set of wealth management, asset allocation, and product structuring tools. The platform integrates these three core functions by being able to automatically generate and execute securities across global markets on multiple asset classes.

Aidyia has developed a cutting edge artificial general intelligence (AGI) technology to identify patterns and predict price movements in global financial markets. AGI is a branch of artificial intelligence aimed at learning mimicking the human brain’s breadth, depth and generality of understanding. Applied to financial markets, the result is financial prediction and trading systems with a human like ability to not only recognize mathematical patterns in market data, but to understand what these patterns mean in a broader context.

Call Levels provides a free app that delivers financial market data updates. Powered by the cloud and built with proprietary monitoring technology, the solution lets everyone access finance information on-the-go at the ease of their fingertips.

Eigencat is a fintech startup supported by the University of Singapore (NUS), which has built a modular digital investment platform for use in the wealth space.

Roboadvice

Roboadvisors are for the mass affluent, and are providing an opportunity to bring together the micro and the macro level of money and engage the mass affluent with a real-time ledger and balance system. I liked the quote from Jon Stein, Founder and CEO of Betterment, who stated that they were not competing with the wealth managers, hence why this is a separate section. He believes their competition is advice versus no advice, and that it is not a battle between robots and humans but a battle between advice and nothing.

In the robo-advisory field, the USA has led the charge with the rise of companies like Wealthfront, Betterment, FutureAdvisor and Personal Capital. They offer wealth management and micro PFM in a killer app. Their features are finely tuned and you can find many comparisons, but this one from Nerd Wallet gives you the low down. These are not the only ones though, as we have folks like Nutmeg over here.

Lending

Peer-to-peer lending is something I’ve blogged about lots here https://finansernextjs.wpengine.com/?s=peer+lending . It’s connecting people who have money with those who need money through software, and mitigating risk through real-time credit analytics. Zopa was the first of these, but many followed including Prosper Marketplace, Lending Club, Lufax and more. I strip out SME Financing from P2P Lending, primarily because it generated a huge new flow of capital to small businesses and start-ups that could not exist without FinTech. However, if you want to know more generally about P2P Lending and related discussions, here are a few blog links worth looking at:

- How peer-to-peer changes the financial world

- At current growth rate, Zopa will dominate >10% of UK consumer lending by 2017

- 10% of lending via P2P?

- The FT picks up our social lending debate

- Marketplace Lending comes of age: arise a new asset class

- Social lending is not so social

- China’s P2P are taking the P

SME Finance

SME Finance is probably the most radical new market that is being changed with technology from peer-to-peer lending to invoice financing to crowdfunding.

Invoice financing often mixes the ideas of peer-to-peer lending with financial factoring and Marketinvoice, a UK firm, is a good example. Marketinvoice launched in 2011 to provide a financial factoring service, which is where a small business can take their outstanding invoices and get them paid early. The firm providing the finance then collects the invoice payment from the client, and takes a commission for having paid the business early. So if I am owed $2,000 by a client who normally pays in 60 days, a factoring firm will offer me $1,800 today and they get $2,000 sixty days later for a $200 or 10% commission. That idea has been around for years, but put it on the internet and a firm like Marketinvoice can grow from lending nothing to lending over £1 billion in five years. This year alone, the firm expects to double that amount, and the difference is that the financing of all of those outstanding invoices is coming from investors. In other words, it is a form of peer-to-peer lending, like the bigger names such as Funding Circle, another SME financing FinTech start-up. Funding Circle provides SME loans, is seven years old and has already funded over £2 billion in loans.

Then there is the new models of crowdfunding. Crowdfunding allows start-up firms to get funding on day one from their potential customers. It used to be that a start-up had to go to a bank to get money to get going. It also had to spend a considerable part of that money on marketing to reach their target audience via media. Sites like Kickstarter, Indiegogo, Crowdcube and Seedrs collapse that start-up structure into one process, where your market and your customers provide you with the funds directly to get going.

This overcomes the issue for banks, who would not fund start-up SMEs because they have no data to analyse to assess the risk of whether funding that SME would result in a return. Where is the market? Will they buy? Crowdfunding businesses turns that risk on its head, as the amount of funding in a crowdfunded business is directly reflected by the demand from the marketplace and customer. In other words, the unknown data the bank is looking for – what is the demand for this product – is determined upfront, before the business gets started, by the potential customer demand. Perfect … except for the Chinese entrepreneurs who steal innovator’s ideas from such sties before they get started.

Nevertheless, the crowdfunders are offering a brand new model of financing that overcomes the issue of lack of data.

Financial Inclusion

Finally, how could we talk about FinTech categories without talking specifically about financial inclusion? This is one of the most exciting areas of FinTech because it brings 4.5 billion people who weren’t worth serving before, because it was too expensive, onto the network. In particular, the financial inclusion programmes in Africa are key, as these are rethinking how money is exchanged through the mobile network. Again, I’ve blogged about this tooooo much, so here’s a quick link to some of the best blogs:

- A world turned on its head

- What is financial inclusion?

- Look at financial inclusion for innovation

- Remittances and the need for financial inclusion

- The unbankable banked

- The challenges of mobile financial inclusion

- Social mobile will make financial inclusion a basic human right

- Which countries are leading financial inclusion?

- UK Financial Inclusion Report Recommends 22 Things For 2020 (Some For Banks)

- Financial Inclusion, Digital Identity and the White House

Chris M Skinner

Chris Skinner is best known as an independent commentator on the financial markets through his blog, TheFinanser.com, as author of the bestselling book Digital Bank, and Chair of the European networking forum the Financial Services Club. He has been voted one of the most influential people in banking by The Financial Brand (as well as one of the best blogs), a FinTech Titan (Next Bank), one of the Fintech Leaders you need to follow (City AM, Deluxe and Jax Finance), as well as one of the Top 40 most influential people in financial technology by the Wall Street Journal's Financial News. To learn more click here...