One company that is seeking global domination is Ant Financial. The company has an open stated intention to reach two billion users by 2025. The way in which they’ll achieve that is through local partnerships, and many of those have been started already:

- Ant Financial invests in Thailand's Ascend Money as part of global expansion play, November 2016

- Alibaba to lead $200 million investment into Paytm’s online marketplace, February 2017

- Jack Ma’s Ant Financial makes first investment in the Philippines, February 2017

- Alibaba’s Ant Financial expands to Korea with $200M investment in Kakao Pay, February 2017

- Globe, Ant Financial form partnership to improve GCash in Indonesia, February 2017

The above partnerships are ones where Ant Financial has a strategic interest. Others are more tactical, and aimed to provide coverage in parts of the world where Chinese tourists can be found:

- Wirecard and Alipay sign agreement for innovative POS payment acceptance, November 2015

- Alibaba’s Ant Financial Strikes Deal With Ingenico for European Payments Push, August 2016

- Ant Financial partners with First Data and Verifone as part of its global expansion, October 2016

And then there are strategic acquisitions, of which the major one under way since January 2017 is Moneygram for remittances. Countered by a bid from Euronet, the acquisition has fallen fallow for a while now, which is why Ant Financial is refiling for review with US decision makers this week to determine the outcome.

All in all, it almost feels as though the firm is moving at lightning speed to build a global prescence. For example, Stripe announced Ant Financial integration with their APIs this week, along with BBVA announcing a rollout of Alipay in Spain. In fact, it almost feels like there is a new strategic or tactical move every single day. Why so much activity? Well, the overall focus is upon inclusivity and to bring the 4.5 billion unbanked and underbanked into Ant Financial's cheap, simple and easy mobile financial ecosystem. It is a laudable ambition and, building upon my blog earlier this week about global FinTech specialist players partnering, Ant Financial is already a long way down that route.

That is why I’ve been in Hangzhou this week, to find out in depth what is happening from those who know. Meantime, if you haven’t been following this closely, here’s a good analysis of what has been going on from Caixin Global, the English version of China Economics & Finance.

Ant Financial Steams Into Uncharted Waters of Global Markets

(Beijing) — China’s largest internet financial-services provider, Ant Financial Services Group, is making mighty strides abroad by forging partnerships in Asia, Europe and the U.S. in a bid to connect its payment service, Alipay, with more customers and merchants globally.

Ant Financial, the former finance arm of e-commerce giant Alibaba Group Holding Ltd., last week announced a partnership with U.S. credit-card processing service First Data Corp., which will allow Alipay users to make payments at the 4 million U.S. merchants served by First Data. The deal came while Ant Financial was pushing for another deal to get a foothold in the global payment market via a $1.2 billion bid for U.S. money-transfer specialist MoneyGram International Inc.

Only one month ago, Ant Financial clinched two other deals in Asia, including an internet finance joint venture with Indonesian media group Elang Mahkota Teknologi (Emtek) and a $1 billion acquisition of Singapore-based payment provider HelloPay. In previous months, Ant Financial made investments in Thailand, Philippines and South Korea to expand its footprint in local payment markets.

“There will be more partnerships in other countries to promote Alipay globally, especially in developing countries,” Jia Hang, Ant Financial’s senior director of international business, said in early May.

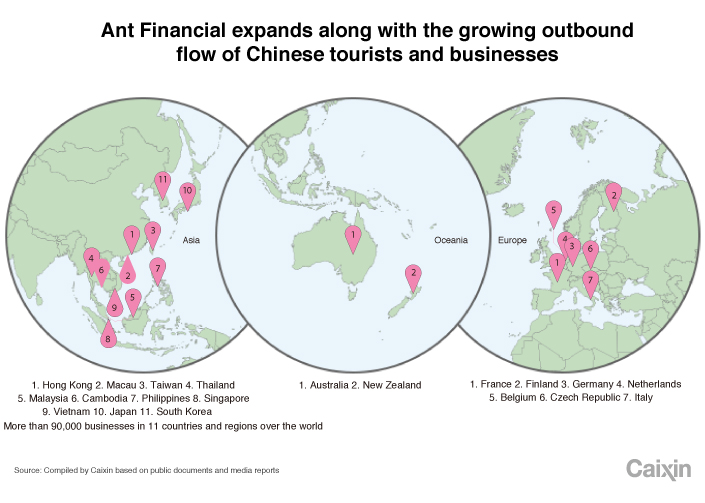

Ant Financial, which is preparing for a public listing that may value the company at more than $75 billion, is picking up steam in overseas expansion along with the growing outbound flows of Chinese tourists and business.

In 2016, Chinese tourists made 122 million outbound trips, spending $109.8 billion overseas, according to a report jointly issued by online travel service provider Ctrip International and the China Tourism Academy (CTA).

The overseas buying spree means lucrative business opportunities for payment providers like Alipay, which is offering services in more than 70 countries and regions to help its users make payments, exchange currencies, and get tax refunds at airports, shopping malls and merchants. The company has set a goal to connect its services with 1 million merchants worldwide in three years.

A Chinese executive of a French retail multinational said Alipay is welcomed in France because about 80% of customers who shop at the country’s luxury shopping malls such as Galeries Lafayette are from China. “Most Chinese prefer mobile payments, so Lafayette will surely accept it,” the executive said.

|

In late April, Finland’s tourist authority held a meeting with major retailers to promote Alipay, which has partnered with Finland’s largest mobile-payment provider, ePassi, to allow Alipay users to make mobile payment in Finland stores. Alexander Yin, chief financial executive of ePassi, said ePassi, which serves 600,000 users in Finland, now has access to Alipay’s 450 million users in China.But Ant Financial’s ambition extends far beyond serving Chinese tourists overseas. Through the partnerships it developed with foreign payment and financial institutions, the company is distributing its technology and business model worldwide and laying the groundwork for a financial-service network that may eventually challenge Visa Inc. and MasterCard Inc.

“Ant Financial’s overseas expansion will not rely on one certain product or capital. It will mainly rely on its technology and customer-service experiences,” Jia said.

As Ant Financial penetrates deeper into overseas financial-service markets, it will also face increasingly complicated tasks concerning different local payment habits, foreign-exchange fluctuations, as well as financial and capital regulatory hurdles, said Chen Zhiyu, an Alibaba overseas e-commerce director. And there will be no one-size-fits-all solution.

Seeking partners

Ant Financial has been counting on local partnerships to spearhead overseas ventures rather than taking the riskier path of going it alone in overseas markets. “Local partners are more familiar with their domestic market, financial industry and regulations in order to make sure the ventures comply with local rules,” Jia said.

According to a source close to Ant Financial, the company acquired minority stakes in most of its recent overseas venture deals in the hope of avoiding possible hurdles to getting financial licenses. But Ant Financial was granted significant minority status in most deals, allowing it to oppose the entry of new investors it doesn’t prefer, the source said.

Ant Financial has been mapping out its overseas strategy since 2015 when the company invested more than $900 million for a 40% stake in Delhi-based One97 Communications, which operates online payment service Paytm. Under the partnership, Ant has provided both cash and technology investment into Paytm and has sent tech support teams to Paytm to help develop products, improve its systems and risk-control capacity, and carry out marketing campaigns.

With the help of Ant Financial, Paytm has enjoyed a tenfold growth over the past two years and became India’s largest payment provider with more than 200 million users and daily transactions exceeding 11 million, while Ant Financial has extended Alipay’s market reach and brought its technology standards to India, including its popular quick-response (QR) code payment technology, which allow consumers to pay for goods and services by scanning a bar code with their mobile devices.

Ant Financial is hoping to replicate the success it developed in India to more countries. In November, Ant Financial announced an investment in Thailand’s Ascend Money, an arm of the agriculture-to-telecom conglomerate Charoen Pokphand Group. Ant Financial will help Ascend build online payment and financial services. Wen Tao, Ant Financial’s tech director in Thailand, said the company has sent a team to help Ascend develop technology and train professionals. Similar partnerships for sharing Ant Financial’s technology and business models have also been adopted in its investments in Indonesia and the Philippines.

Challenges ahead

As business expands into more regions, Ant Financial is seeking to enhance its cross-border money-transfer capacity. In April, the company increased by 36% a cash offer for U.S. money-transfer specialist MoneyGram International, to $1.2 billion, topping rival bidder Euronet Worldwide Inc.

The transaction still needs U.S. regulatory approvals. A source close to the matter told Caixin that “MoneyGram is very important for Ant Financial” in its overseas expansion, as the U.S. firm’s cross-border remittance business will fill a hole in Ant Financial’s international operations. MoneyGram has more than 350,000 locations in 200 countries and a network of 2.4 billion bank and mobile accounts around the world.

Currently, Alipay’s cross-border money transfers are handled mainly by China Construction Bank and Citic Bank, which jointly settled $6 billion in overseas remittances for Alipay in 2016, according to sources close to the company.

Expanding cross-border cash flows have fueled risk concerns. A bank executive said each money transfer handled by banks for Alipay is usually packed with thousands of small transactions involving numerous individuals and small vendors, which poses a great challenge for banks to check the authenticity of every transaction.

“Some of these transactions may involve money laundering risks,” the bank executive said.

Last week, the central bank imposed 30,000 yuan ($4,300) fines on Alipay and its major rival, Tenpay, operated by messaging giant Tencent Holdings Ltd., for failing to ensure that at least 90% of its users are registered with real identification based on the rule set by a 2016 document for non-bank payment companies.

“Theoretically, even 0.1% of accounts that are not registered with a real name can create an opportunity for money laundering,” a bank employee said.

The surge of cross-border payments made by Alipay is also a difficult task for regulators to supervise, according to capital-flow rules. China’s foreign-exchange regulator currently requires each individual to exchange no more than the equivalent of $50,000 in foreign currencies each year.

A central bank official told Caixin that cross-border payments handled by internet payment providers involve money transfers of the yuan and foreign currencies, which are overseen by separated departments of the central bank, as well as the State Foreign Exchange Administration. In light of the fast growth of online cross-border money transfers, the central bank is considering unifying regulatory responsibility to enhance supervision, the official said.

Despite looming financial security and regulatory concerns, Ant Financial is facing heated competition overseas as more rivals flood into the market.

Alipay archrival Tenpay, which offers payment and various financial services through Tencent’s popular messaging app WeChat, now operates in 12 countries, supporting transactions using 10 currencies, compared to 18 for Alipay. Since late last year, Tencent has invested in India’s e-commerce platform Flipkart and social networking app Hike Messenger in the hopes of introducing Tenpay into India.

Greater challenges may come from traditional payment market giants, such as China UnionPay, Visa and MasterCard, which are gearing up their efforts to tap into the mobile-payment market. China UnionPay, the country’s sole bank-card association, has partnered with 17 commercial banks and 2 million merchants in China to promote its own version of QR-code payments and get a share of a market that has been dominated by Alipay and Tenpay.

In May, China UnionPay joined with Visa and MasterCard to develop the official QR-code payment standards for Thailand, shortly after Visa and MasterCard partnered with India’s RuPay to release a national QR-code standard in India, which is different from Ant Financial’s.

Analysts expect bank-card associations’ foray into QR-code payments will bring profound changes to the market as their models are believed to be more transparent and secure compared to the lingering security concerns of services provided by payment companies.

“Regulators in many countries haven’t got time to evaluable and think about the changes Ant Financial will bring to local payment industry. What they see now is immediate profit,” a source at Visa said.

Contact reporter Han Wei (weihan@caixin.com)

Chris M Skinner

Chris Skinner is best known as an independent commentator on the financial markets through his blog, TheFinanser.com, as author of the bestselling book Digital Bank, and Chair of the European networking forum the Financial Services Club. He has been voted one of the most influential people in banking by The Financial Brand (as well as one of the best blogs), a FinTech Titan (Next Bank), one of the Fintech Leaders you need to follow (City AM, Deluxe and Jax Finance), as well as one of the Top 40 most influential people in financial technology by the Wall Street Journal's Financial News. To learn more click here...