I've written a column for The Banker magazine for the last 15 years and, during that time, have collected their special July edition each year. Every July The Banker publishes their analysis of the Top 1000 banks in the world. In the 1990s, the top 10 were mainly Japanese; in the 2000s, American; and today, Chinese. This year is particularly interesting as there is a clear impact of Brexit on the British banks. Here's the summary.

BOOM FOR FRENCH BANKS AS BREXIT DAMAGES BRITISH RIVALS

3 July 2017: The fallout from Brexit has pushed the UK’s leading banks further down The Banker’s latest ranking of the Top 1000 banks. UK banks made less than half the profits compared to French banks and the gap is likely to widen with a Macron business boost expected across the Channel.

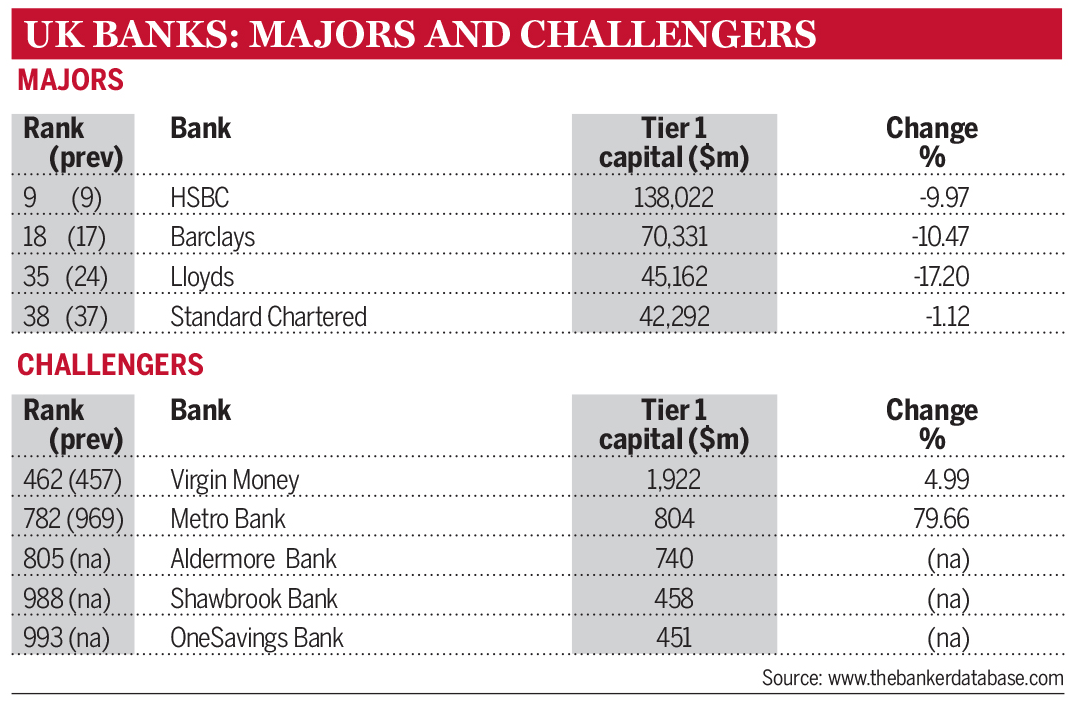

Uncertainty following the EU referendum, coupled with a drop in the value of sterling, sent domestic-focused banks tumbling in the ranking. The Royal Bank of Scotland fell from 19th to 30th and Lloyds fell from 24th to 35th in the ranking, which uses Tier 1 capital as its key measure.

The ranking showed that internationally focused UK banks such as HSBC also fared badly. Despite holding on to 9th position, they suffered a 62% fall in profits, making this their worst result in seven years. HSBC previously topped the ranking in 2008.

In the 2007 ranking, UK banks collectively made $17.3bn in pre-tax profits, a 32% fall on the previous year, and approximately a quarter of what they made before the financial crisis. In 2008, UK banks delivered 10% of global banking profits; however, that contribution has shrunk to 1.80%. In contrast, French banks made $39.6bn in profits, double that of UK banks.

The Banker’s editor Brian Caplen said: “Brexit has dealt another blow to the UK banking sector, which was already struggling due to issues caused by the financial crisis and various other scandals. At the same time, French banks are shaping up as the strongest in Europe and the outlook for them is even more positive with pro-business Emmanuel Macron in the Élysée Palace.”

There is some good news for the UK banking sector from the challenger banks. Metro Bank rose 187 places from 969th to 782st with an 80% capital increase, although it is still making losses. Two challenger backs also entered the ranking for the first time: Aldermore at 805 and OneSavings at 993. Shawbrook returned to the ranking at 988.

While the performance of UK banks is less than stellar, they are doing better than some other European countries. Italy chalked up the largest country losses ($16.3bn) followed by Portugal ($3.7bn) and Greece ($3bn).

Italy’s UniCredit fell 16 places in the overall ranking to 45th. It recorded the highest losses of any bank ($10.9bn) and three other Italian banks feature in the Top 10 highest losses table.

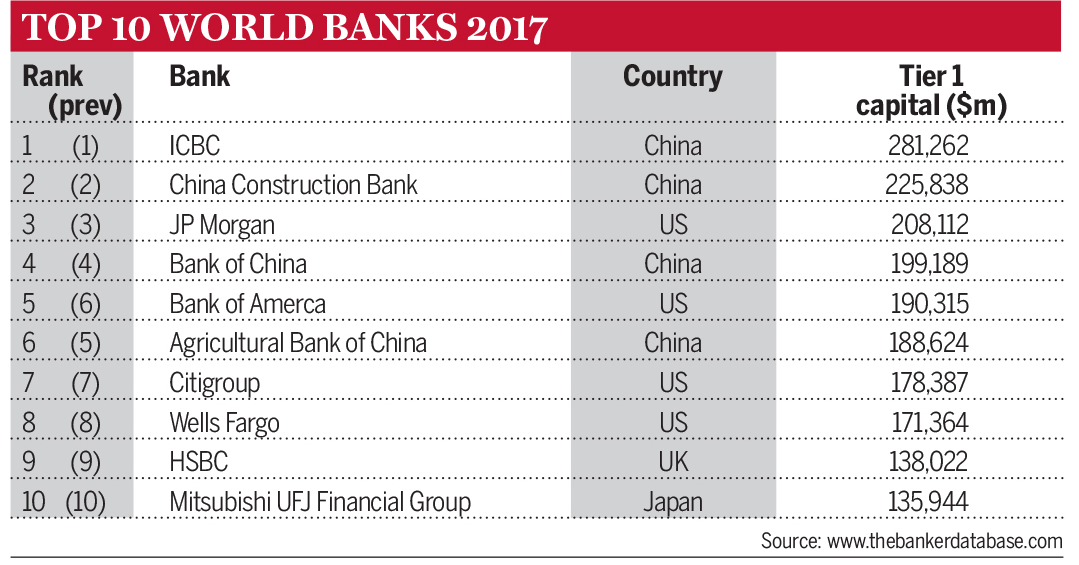

Chinese banks still dominate the ranking although the top five Chinese banks saw their profits fall as the economy slowed down. Industrial and Commercial Bank of China (ICBC) came top for the fifth year running with $281bn in capital.

Banks in the other BRIC countries witnessed notable profit increases, including Russia (369%), Brazil (179%) and India (26%).

Oh, and editor-in-chief of The Banker Brian Caplen talks through the results here (7m35s):

And further details from the July issue below:

THE 2017 TOP 1000 BANKS LIST by Danielle Myles:

With capital levels now under control, The Banker's Top 1000 World Banks ranking shows that the global banking sector’s biggest problem is profitability. Emerging market lenders have proven resilient to the commodity crunch and their national crises, but their European rivals are struggling, and there is more than interest rates to blame. By Danielle Myles.

The latest Top 1000 results suggest the Basel Committee has much to be pleased about. The aggregate Tier 1 capital of banks in this year’s rankings has jumped 3.85%, meaning the global banking sector holds 72% more capital than at the outbreak of the global financial crisis in 2008.

To be included in the 2017 edition of the Top 1000, banks must hold at least $442.12m in Tier 1 capital, $38m higher than 2016’s entry threshold. It is the third biggest increase in a decade, topped only by the 2013 and 2014 rankings, when banks were scrambling to satisfy new capital requirements under the first phase of Basel III.

Even more impressive is that this occurred despite currency depreciation. The Banker’s Top 1000 methodology converts all figures to US dollars to create a comparable ranking. However, as most banks report in their local currency, their figures can be materially affected by foreign exchange moves. The US Dollar Index hitting a decade-high in 2016 has artificially deflated non-US banks’ Tier 1 capital (as reported in the Top 1000), but nonetheless, capitalisation has still spiked.

More evidence of the robustness of banks’ balance sheets is found in the capital-to-asset ratio. This is similar to Basel’s 3% minimum leverage ratio, except that The Banker’s metric excludes off-balance-sheet items. Many banks detest the leverage ratio as a blunt tool that does not distinguish between super-safe assets, such as AAA rated government bonds, and high-yield notes. Yet based on the global aggregate capital-to-assets ratio hitting 6.5%, they seem to be finding a way to satisfy it.

All this may please policy-makers, but for the industry their problems have simply moved on from a lack of safety and soundness, to a lack of profitability. Global pre-tax profits slid once again in 2016, this time by 1.21%, yet there is little uniformity around the world.

Once again, Africa’s return on assets (ROA) is higher than any other region. Its return on equity (ROE) and return on capital (ROC) are second to Latin America, but excluding crisis-ridden Venezuela (where results are distorted by triple-digit inflation and a drastically overvalued official exchange rate), Africa sweeps the board for profitability indicators.

Asia-Pacific still accounts for the lion’s share of global profits, but over the past four years North America has chipped away at its dominance. With the US Federal Reserve on course to lift interest rates to 1.5% by the end of 2017, the trend looks set to continue into next year’s rankings. Other regions, however, are battling significant macro-economic headwinds, and with varying success.

Middle East weathers the oil crisis

One of the most striking takeaways from this year’s Top 1000 is the Middle East’s resilience to the collapse in oil prices. The oil rout began in 2014 but fears for its banks took hold early in 2016 when the price per barrel dipped below $30.

Credit rating agencies responded by downgrading sovereigns and banks across the region, while oil-dependent governments slashed spending, funding costs increased and more borrowers became at risk of default. Analysts predicted turmoil for banks in the Gulf states, warning about lower profitability, higher non-performing loans (NPLs) and impairment charges, a liquidity crunch and resultant industry consolidation.

But this year’s rankings suggest that the oil price collapse has not had the catastrophic effect predicted. Regional aggregate profits slid 4.4% from 2015, but are still higher than 2014 and 2013, when oil hovered around the $100 per barrel mark. Regional ROA is flat at 1.51%, while ROE is 12.23% – more than double that of western Europe. By almost every measure, the Middle East was more profitable in 2016 than four years prior.

Analysing the region’s biggest banking and oil-exporting markets shows the trend also holds up on a national level. From 2013 to 2016, Saudi Arabian banks’ profits have grown 9.8% while those of the United Arab Emirates and Qatar are up 26.6% and 20.8%, respectively. Kuwait and Bahrain have also increased returns in the years since crude prices started to slide.

Other signs of a sector in distress have not materialised either. There has been just one merger, between National Bank of Abu Dhabi and First Gulf Bank (FGB) – the UAE’s second and third biggest lenders – to create First Abu Dhabi Bank. The deal was motivated by their complementary strengths in retail and investment banking, not to shore up struggling balance sheets.

The Middle East’s aggregate Tier 1 capital is steady and in 2016 its biggest lender, Qatar National Bank, grew headcount by 85% and capital by 21% to move up the rankings from 89th to 83rd. Middle East deposits in general did shrink by 9% in 2016 and the loan-to-deposit ratio edged up 7%, but this is far from the liquidity crunch many feared. All in all, it suggests that banks are leading the charge in breaking Gulf states’ oil dependency.

Western Europe’s share of global profits has shrunk by 2.78 percentage points, but this belies the depth of its woes. It is home to three of only four countries to record a 2016 loss, as well as the year’s 11 biggest loss-making banks. By The Banker’s three main profitability indicators – ROA, ROE and ROC – western Europe now lags far behind all other regions. It is important to note these ratios have declined from 2015 to 2016 not because of a rise in their respective denominators – in fact, the region’s assets, equity and Tier 1 capital fell last year, broadly in line with the euro’s 3.3% depreciation. The culprit is pre-tax profits (their common data point), which have slid more than 17% to $125.6bn.

Profits in each of the region’s biggest banking markets shrunk in 2016. Many CEOs pointed to low interest margins – the difference between interest charged to borrowers and paid to depositors – which they blame on the European Central Bank (ECB) and Bank of England cutting rates to historic lows in 2016. But profitability differs greatly from country to country, suggesting other factors are at play.

The worst offender is Italy, which recorded a $16.3bn loss. Half of its banks in this year’s ranking made a loss, but the nationwide drop is caused by a select few: namely Banca Popolare di Vicenza and Veneto Banca, which will be wound down after the ECB confirmed they were failing, and four of the country’s six biggest banks.

Monte dei Paschi’s problems are now well known, but the more notable name is UniCredit; its $10.88bn loss is more than double that of any other bank in this year’s Top 1000. Its capitalisation has been hit too, prompting a slide from 31st to 45th in the overall rankings while losing its status as Italy’s biggest bank to Intesa Sanpaolo. However, in the fourth quarter of 2016 UniCredit did record €12.2bn in one-off charges to clean up its balance sheet, and earlier this year it completed a €13bn rights issue, so the bank could rebound in next year’s rankings.

Portugal has experienced a similar situation. Sector-wide losses have ballooned from $391m to $3.65bn, largely due to the fortunes of its biggest name. Caixa Geral de Depositos has posted the sixth biggest loss in this year’s rankings and dropped nearly 100 places to become the country’s third biggest lender. The success of the €5bn recapitalisation package it agreed with EU authorities and the Portuguese government will not be known until next year’s rankings.

Europe’s stabilisers

The powerhouse of European banking is now France. Only six of its lenders appear in the Top 1000 but they account for nearly 18% of Tier 1 capital and 26.7% of profits recorded in western European balance sheets in 2016. This supports claims that consolidation in Europe’s fragmented and overbanked countries, namely Italy and Germany, would see an improvement in profitability. The mid-size banking sectors doing their best to keep regional returns afloat are in Belgium and Austria – where profits are up between 15% and 20% – and Poland and Denmark, where they have grown 33%.

Greece’s fortunes are slowly improving. The capital cushions of its five banks in this year’s rankings have slipped a little, but their capital adequacy ratios are above 14.8% and the sector is making progress in repaying the eurozone bailout fund. Collectively their losses shrunk 78.8%, giving Greece a stronger ROE and ROC than Italy and Portugal.

Greece is also home to two of the year’s biggest turnaround stories. In 2015, Alpha Bank and Eurobank Ergasias recorded the world’s fifth and sixth largest losses, yet in 2016 they posted a profit (the latter being its first in six years), and rank first and third in this year’s table of biggest moves from loss to profit.

There is little movement on Germany’s profits, which are being held back by its two loss-makers: Nord LB and Deutsche Bank. For beleaguered national champion Deutsche Bank, 2016 may seem a year to forget, thanks to a painful restructure, speculation it would miss coupon payments on contingent convertible bonds, and a US stress-test failure. But Deutsche has maintained its number 21 global ranking and its capital adequacy ratio is higher than most banks in the top 20. Its pre-tax loss of $852.6m – largely attributable to the $7.2bn spent settling US mis-selling claims from the crisis era – is a fraction of the $6.63bn loss recorded in 2015.

UniCredit may dwarf every other loss in this year’s rankings, but at least it is not a repeat offender like Credit Suisse and RBS. The Swiss bank’s $2.22bn loss is partly attributable to its own $5.28bn settlement with US authorities, but it follows a similar result in 2015, placing significant pressure on its CEO’s turnaround plan.

RBS, which is still 73% owned by the UK government after its 2008 bailout, chalked up its eighth consecutive year without a profit. It looks set to build on this feat next year, as its clean-up and restructure has continued into 2017.

One name our rankings will not be seeing again is second biggest loss-maker Banco Popular. In June 2017, Santander agreed to buy its struggling Spanish competitor for €1 after EU authorities declared it was failing or likely to fail. A notable new name is Germany’s Nord LB, which reported a $1.96bn loss largely due to higher provisioning for its troubled shipping finance portfolio.

US and China’s mid-tier engines

US and Chinese banks have retained their dominance, each accounting for four of the top eight spots in the Top 1000. The only change to the leaderboard sees Bank of America move from fifth to sixth at the expense of Agricultural Bank of China. But on the whole, in 2016 Asia’s rising superpower cemented its status as the world’s biggest banking market by assets and Tier 1 capital, pulling further away from the US, which remains runner-up by both measures.

Nonetheless, the US continued its unassailable post-crisis recovery, posting solid but sustainable growth in total assets, capital and profits. Mid-cap names made the strongest gains, the largest being KeyCorp and Huntington Bancshares. The Ohio-headquartered pair grew Tier 1 capital by between 30% and 40% after acquiring smaller rivals. Once again, the US has more banks in the Top 1000 than any other country; of its 10 new arrivals, the standout is Citizens Bank, debuting at number 99 after being sold by RBS in 2015.

The headline change in China, as in the US, is that growth is now fuelled by second-tier banks. Since hitting a high of 31.1% in the 2014 rankings, sector-wide Tier 1 growth has decelerated at roughly the same rate as its big four banks (ICBC, China Construction Bank, Bank of China and Agricultural Bank of China). In the 2015 rankings, the sector and the big four grew by about 20%, while in last year’s rankings this figure was circa 10%.

However, in this year’s rankings, the big four have grown by less than 2% while the sector is 5.66% bigger. This suggests the leading banks are reaching their size limit, while a number of second-tier lenders – and even more outside the global top 50 – continue to post double-digit growth.

China’s ascent is in sharp contrast to Asia’s other major market, Japan. By every measure, the Chinese banking sector is more than twice as profitable as Japan’s, which has been squeezed by the Bank of Japan’s continued aggressive monetary policy. In January 2016, it took the historic decision to move into negative territory, dropping rates to -0.1%. Net interest income at its biggest four lenders dropped 6.94% from 2015 to 2016, but this does not fully explain the 11.3% drop in overall profits.

There are signs of encouragement though. Of the 90 banks in the Top 1000 only one posted a loss, and Sumitomo Mitsui Financial Group has leapfrogged Crédit Agricole, BNP Paribas and Goldman Sachs to place 12th in the overall rankings.

BRICs bounce back

This year’s Top 1000 gives cause to herald the return of the BRIC (Brazil, Russian, India and China) banks. The emerging market acronym has fallen by the wayside in recent years, as China's and India’s economies soldiered on while Brazil and Russia endured their worst recessions in decades. Yet 2016 marked a reversal of fortunes for the two laggard countries, helping their banks to stage a comeback.

Profits at the 11 Brazilian banks in the rankings surged 179.4%, up from the $10.5bn posted in 2015. Meanwhile, Russian banks’ profits are up 369% to post a total of $14.65bn. Their standouts are Banco BTG Pactual and Gazprombank, which posted among the biggest five moves from loss to profit in this year’s rankings.

These figures have been boosted by foreign exchange fluctuations. The real and rouble were the best performing emerging market currencies of 2016, gaining 16.4% and 16.8% respectively against the dollar (the reference currency for compiling the Top 1000). However, as neither Brazil nor Russia’s currency has recovered to normalised levels, their banks’ strong profit performance is not down to foreign exchange moves alone. This is supported by their profitability ratios, which are not impacted by currency fluctuation. Based on Brazil’s improved ROA and ROC, its banking sector is now more profitable than China’s, while Russia’s ROA is nearly double the global average.

Their rebound is not limited to profits. Of the 16 Russian banks in this year’s Top 1000, 13 posted capital growth that outstrips the rouble’s gains. Its biggest lender, Sberbank, has soared 15 spots to place 36th in the global rankings. Russia’s improving capitalisation was apparent in last year’s Top 1000, when Tier 1 and assets shrunk far less than the rouble’s collapse. It seems no coincidence that its improvement coincides with the central bank’s efforts to clean up the sector. From 2014 to 2016, the regulator withdrew more than 300 banking licences from institutions that were chronically weak or unscrupulously led.

Brazil’s banks weathered its economic crisis better than Russia’s, so there’s been little need to shore up its capital base. Nonetheless, Tier 1 capital at its biggest bank, Itaú Unibanco, grew 37.33%, more than recouping its 28.52% drop the year before.

India’s profitability continues to be hit by rising impairment charges and provisions (ICP), the loss recognised on loan books to account for NPLs and other impaired assets. This process started in 2015 on the central bank’s instruction to clean up balance sheets, and was a major cause of the sector’s profit slump in last year’s rankings. The exercise will continue for some time, but profits edged up in 2016 and three Indian banks – Bank of Boroda, Punjab National Bank and Canara Bank – are among the year’s 10 biggest recoveries.

While Brazil and Russia have been bolstered by their recovering currencies, the UK has experienced the opposite effect. Sterling was the year’s worst performing G-10 currency, finishing 20.9% down against the dollar after dipping to a 31-year low in June sparked by the UK’s surprise referendum decision to leave the EU. It comes as no surprise, therefore, that British bank rankings are the most affected by foreign exchange swings.

But for sterling’s collapse, Barclays would have risen from 17th to 15th, while RBS would have declined just one spot to 20th and Lloyds two spots to 26th. Mid-size banks and building societies were also hit. The two notable exceptions are HSBC and Standard Chartered. As they report in US dollars, and because such a large portion of their revenues is booked outside the UK, their results have not been impacted in the manner of their national peers.

Undoubtedly, Brexit has had a significant effect on this year’s rankings, but some banks have prevailed. Barclays and Lloyds increased profits by 64% and 113%, respectively, while two UK challenger banks have entered the Top 1000 for the first time.

Turkey’s banking market was hit equally hard by foreign exchange. If the lira had not lost 21% against the dollar in 2016, its five biggest banks would have climbed, rather than fallen, in this year’s rankings. It is also why the country has posted the fifth biggest drop in total assets. Angola, Nigeria and Mexico can cite the same reason for appearing on the list of biggest asset declines.

Currency depreciation may also be why Egyptian and Nigerian names have experienced some of the biggest declines in deposit funding. However, in this case, it has had a tangible impact on their business. Their central banks relaxed or scrapped their pegs against the dollar in 2016, causing the Egyptian pound and naira to plummet. Depositors would be forgiven for withdrawing their cash to convert into more stable currencies, rather than simply losing value sitting in the bank.

As an investment bank, Banco BTG Pactual has historically relied on wholesale funding. However, its deposits nearly halved in 2015, and again in 2016, as customers reportedly rushed to withdraw their cash following the arrest of its CEO as part of Brazil’s wide-ranging corruption inquiry. André Esteves resigned as CEO and has still not been charged. He denies any wrongdoing.

HSBC still runs the world’s most formidable overseas network, with its 18 foreign-owned subsidiaries (FOS) generating nearly three times as much profit as the firm as a whole in 2016. The Hong Kong business – its engine – is twice as profitable as any other FOS in the world, although Bank of China’s (BoC) local subsidiary is gaining ground. Its profits more than doubled in 2016 to $7.9bn, pushing BoC up to fourth in the list of best-performing foreign networks. While other Chinese banks have aggressively expanded overseas in recent years, they have done so via branches and so are notably absent from the FOS rankings

Banco Santander comfortably retains second place in the list of most profitable foreign networks. Its FOSs now mirror HSBC’s efforts in posting a bigger profit than the parent. This is largely thanks to its Brazilian business which, after dropping out the top 25 FOS list last year, has staged an impressive comeback to rank third. It is consolation for Santander’s US business, which has tumbled since two years ago when its profits were second only to HSBC Hong Kong.

One overseas network to watch is Mitsubishi UFJ Financial Group. Profits at its Americas business doubled in 2016 and the Japanese parent is investing heavily in its European operations. Spain’s BBVA should also continue to grow overseas profits, having upped its stake in Turkey’s biggest bank, Turkiye Garanti Bankasi (which is now deemed a subsidiary), while its Mexican subsidiary remains a solid performer. A network likely to disappear is Nordea, which recently converted many of its subsidiaries into branches, including its top-performing Finnish business.

Asset quality

Western Europe’s dominance of the ranking for ICP reveals this to be one factor behind the region’s woeful profit performance. But while higher ICPs are putting short-term pressure on returns, they are part of the necessary process of addressing NPLs. As such, it is encouraging to see Europe’s four worst offenders for NPLs – Greece, Portugal, Italy and Cyprus – setting aside more ICPs (as a percentage of their operating income) than any other countries in the world.

While Portugal and Italy’s ICP-to-income ratios are on the way up, Cyprus and Greece are heading in the opposite direction, suggesting the quality of their loan books may be improving. Greece’s ratio reduced 125.6 basis points in 2016, which partly explains why its loss has shrunk nearly 80%.

CEOs’ efforts to reduce the riskiness of their asset base – in order to keep capital requirements in check – have started to pay off. The Top 1000’s risk-weighted asset (RWA) density (RWA-to-total assets) fell for the first time in two years. European and Japanese banks continue to have the lowest RWA densities, partly caused by their retreat from capital-intensive businesses to boost profitability.

However, banks from these regions favour internal models to measure risk, a practice the Basel Committee is considering curbing. If Basel follows through on the proposed changes, Japan and Europe’s RWA densities may start heading north.

In recent years, big European banks have posted the most significant falls in RWA, but in this year’s ranking they are notably absent. It suggests they may, by and large, have finished their major de-risking exercises.

Big European and US banks continue to set the benchmark for cutting headcount, as rising regulatory costs force them to improve efficiencies to boost profits. Citigroup recently announced that its multi-year restructure is over, so its downsizing may be drawing to an end. UniCredit, on the other hand, is upping the ante. After steadily shrinking headcount since 2010, last year it axed 15.64% of its workforce and announced a new strategic plan that involves slashing 14,000 jobs by 2019.

Somewhat surprisingly, European-headquartered banks set the pace for hiring. BBVA’s number two ranking is due to its acquisition of CatalunyaBanc and Turkiye Garanti Bankasi’s new classification as a subsidiary. But the year’s big story is Home Credit. The 585th-ranked Dutch bank sells small short-term loans for household items to customers with little or no credit history. In 2016 its headcount soared 65% after bulking up in India, China and Indonesia.

Another surprise is that Qatar National Bank, the Middle East’s biggest bank, has more than doubled its staff since the beginning of the oil rout in 2014. It added 85% more employees last year alone, although this may be partly down to its acquisition of National Bank of Greece’s Turkish subsidiary Finansbank.

Russia’s biggest lender, Sberbank, shed more than 5000 jobs in 2016, but its exponential rise in staff numbers over the 24 months prior means it still ranks fourth in the list of biggest hirers. Meanwhile, Chinese banks’ headcount is still growing but, as with their capital levels, at a slower rate than previously. Two years ago they claimed eight of the top 10 spots for rising headcount, but this year there are only three names.

Postal Savings Bank of China is an interesting exception. It cut nearly 10% of its workforce in 2016, a much-needed measure given it had three times as many employees as similar-sized Chinese banks. It became a public company in September 2016, so may face more pressure to improve efficiencies and accountability, and therefore downsize more swiftly going forward.

It is striking that the biggest increases in employee numbers are significantly lower than a few years ago, suggesting the biggest banks are not only reaching their natural limit in terms of capital and assets, but also of their workforce.

It was a relatively uneventful year for bank mergers and acquisitions, but some deals that completed in 2017 will affect next year’s rankings. First Abu Dhabi Bank, formed by the merger of National Abu Dhabi Bank and FGB, is set to become the UAE’s biggest bank. Meanwhile, based on their combined Tier 1 capital at the end of 2016 (without adjustments), Santander’s takeover of Banco Popular should see Spain’s biggest bank jump a few places up the rankings.

Chris M Skinner

Chris Skinner is best known as an independent commentator on the financial markets through his blog, TheFinanser.com, as author of the bestselling book Digital Bank, and Chair of the European networking forum the Financial Services Club. He has been voted one of the most influential people in banking by The Financial Brand (as well as one of the best blogs), a FinTech Titan (Next Bank), one of the Fintech Leaders you need to follow (City AM, Deluxe and Jax Finance), as well as one of the Top 40 most influential people in financial technology by the Wall Street Journal's Financial News. To learn more click here...