I’ve got caught in a few discussions recently with people who tell me Ant Financial are Chinese. They’re not. Neither is Alibaba and, if you think they’re just Chinese, you’re going to miss a huge change in the next decade. Ant Financial is an open marketplace of apps, APIs and analytics, that I’ve been describing for a while as the Open Sourced Financial Marketplace. They got the idea before many others and, unlike many others, have the billions of dollars to make it happen on a globalised basis.

I see this, and it is why I picked on them as the 30,000 word case study for ‘Digital Human’, as they’re the only company in the world today acting on a marketplace of financial inclusion globally. PayTM in India is powered by many of Ant Financial’s apps and APIs, as is Globe Telecom’s GCash in the Philippines, Ascent Money in Thailand, Easypaisa in Pakistan and many more. Equally, through partnerships with Ingenico, Wirecard, First Data and more, they are offering easy payments through QR codes to Chinese tourists across America and Europe and, if you think it’s just for Chinese tourists, then you’re also wrong.

In fact, it amazes me how short-sighted some folks are. For example, I had a LinkedIn run-in the other day.

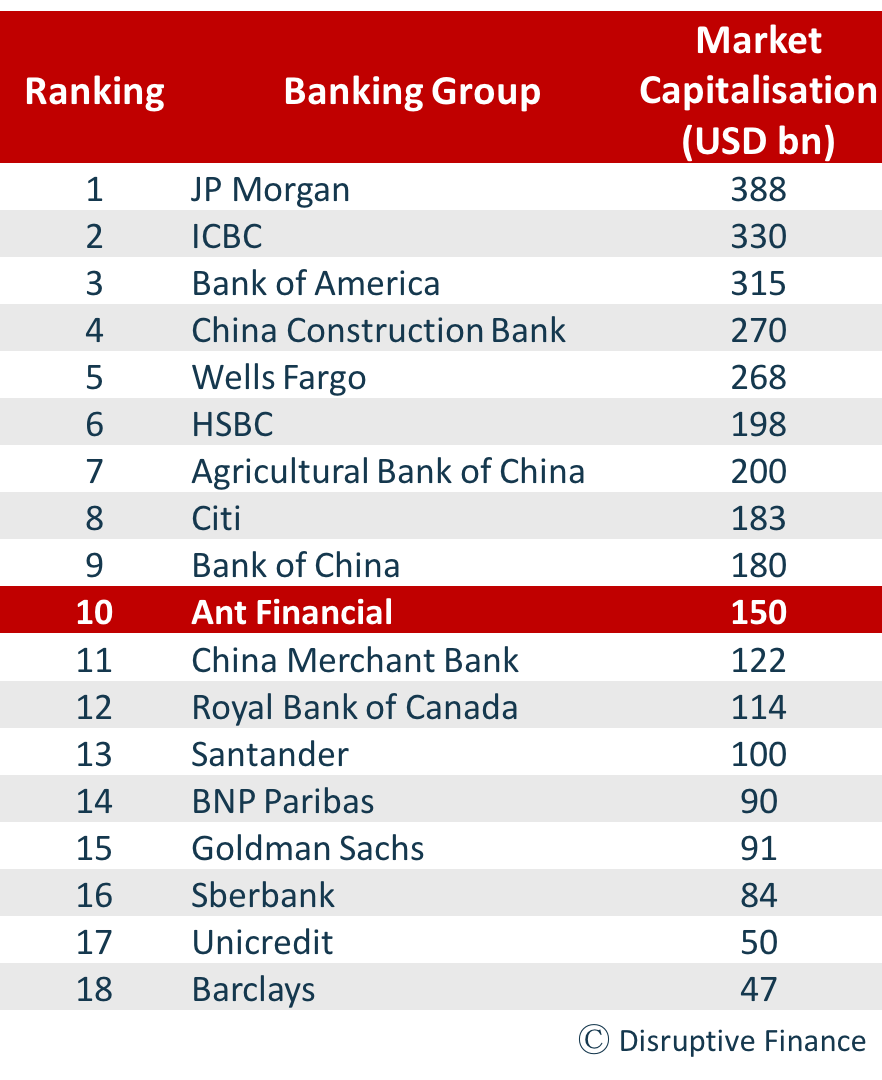

It all started with a very good sum-up of Ant Financial’s recent $150 billion by Huy Nguyen Trieu, CEO @ The Disruptive Group. Ant were valued at around $50 billion when I first started to focus upon them two years ago, so a tripling in value in two years is notable, especially as it would make them the tenth largest bank in the world by value.

That is what Huy was writing about:

If one removed the reference to Ant Financial, it wouldn’t look like a Fintech company, but a diversified financial institution of very large scale – which it is. From payment to wealth management, lending, insurance, and even its own credit scoring agency, Ant Financial is simply a major financial institution.

Of course, this is not a normal financial institution. If only because it was created 14 years ago, and not 200 years ago like some traditional banks. And it is before all a tech company that grew to become a financial institution. From a $50bn valuation two and a half years ago, it has now reached $150bn last month.

So, a guy called Kelvin (some dude in Standard Chartered Bank https://www.linkedin.com/in/kelvin-tan-6990844/ ) commented: Yes. But because of their size in a single country on LinkedIn.

I took exception to this, as I clearly know from writing the case study and the focus of Ant that they are not in a single country but global. So, I replied:

They’re global, not Chinese .... see 30,000 word case study in ‘Digital Human’

Kelvin decided to take me up on the case: perhaps. I wonder how much of their assets and liabilities are in china / chinese nationals

Chris: increasingly less when you look at what they’re doing with Paytm, Easypaisa, Globe Telecom and other partners in Philippines, Thailand, Korea etc. No ‘perhaps’ about it

Kelvin: are you talking about investments in these areas or actually building out full wallet propositions? What % do they constitute if the latter?

Chris: full wallet partnerships. Represents almost half of value (guess)

Kelvin: I think your guess is waaayyy off :)

Chris:

Suit yourself. I know them better than you and their $50bn valuation two years ago is when they were big in China. Now they’re big everywhere and worth $150bn, even though they are smaller in China as WeChat Pay grows. Do the math and look at what they’ve done last two years, and my statement makes 1000% sense. But if you know them better than I do and have written more than 30,000 words as a case study on them, I’m happy to be persuaded otherwise. P.S. read ‘Digital Human’ and its’ Ant case study before replying

It's interesting how many people who have little knowledge of Ant Financial, Alipay and Alibaba think they know them well when they don’t. they’ve stereotyped them as being Chinese and focused upon China, when they’re not focused just on China but on being global. In fact, it’s at the heart of the Alibaba Group’s mission to be global as set out in the original pitch for the idea by Jack Ma back in 1999:

In case you can’t play the video, here’s Jack’s vision of twenty years ago:

First, we should position Alibaba as a global website, not just a domestic website.

Second, we need to learn the hard-working spirit of Silicon Valley. If we go to work at 8am and go home at 5pm, this is not a high-tech company and Alibaba will never be successful. If we have that kind of 8am to 5pm spirit, then we should just go and do something else.

Americans are strong at hardware and systems. But on information and software, Chinese brains are just as good as theirs. All of our brains are just as good as theirs. This is the reason we dare to compete with the Americans.

If we are a good team and know what we want to do, one of us can defeat ten of them. We can beat government agencies and big famous companies because of our innovative spirit. Otherwise, what is the difference between us and them?

So, my first point is that anyone who thinks Alibaba, Ant and Alipay is just a Chinese firm focused on Chinese citizens has got their head up their arse.

Second point is that valuation of $150 billion. In another conversation on social media, someone questioned that valuation (coincidentally a former member of Standard Chartered, Axel Winter, Former Global Chief Architect & Technology Strategy Head).

I happened to post an update:

Alibaba $500 billion. Ant Financial $150 billion. Jack Ma priceless. #Alipay

— Chris Skinner (@Chris_Skinner) May 27, 2018

And linked to Huy’s article. Quite rightly Axel pointed out that valuations of pre-IPO tech unicorns are very different to those of established players, as it’s linked to their future potential rather than actual delivery. I agreed and linked to this important Harvard Business Review article on tech company valuations:

Why Financial Statements Don’t Work for Digital Companies, by Vijay Govindarajan, Shivaram Rajgopal and Anup Srivastava who conclude that “our current financial accounting model cannot capture the principle value creator for digital companies: increasing return to scale on intangible investments”.

The article is well worth a read, but it does bring home the importance of these new digital platforms and marketplaces. They are not being valued on assets but expectations. And my expectation is that Ant Financial will rival Alibaba’s value in a few years, just as PayPal did with eBay. A great illustration of this is the latest news I got from Ant Financial this week:

Ant Financial to support Shanghai Pudong Development Bank’s digital transformation with financial-grade technologies

Partnership is third of its kind announced this month between Ant Financial and established banks

HANGZHOU, May 30, 2018 – Ant Financial Services Group (“Ant Financial”) has signed a strategic cooperation agreement with Shanghai Pudong Development Bank Co., Ltd. (“SPD Bank”) to support the bank’s digital transformation with Ant Financial's technological capabilities. The agreement is the third of its kind announced this month between Ant Financial and established banks, following partnerships with Huaxia Bank and China Everbright Bank.

Ant Financial and SPD Bank will partner in online risk management, including fraud prevention, with the former providing technological support to help the latter prevent loan, transaction and marketing fraud. The partnership will also leverage Ant’s financial-grade technologies in AI, supply chain finance, biometric identification and risk management.

“Ant Financial and SPD Bank share the same vision for the future. With this partnership, we will explore how to improve efficiency in banking operations, as well as how to leverage technology to create greater value for our users,” said Eric Jing, Executive Chairman and CEO of Ant Financial.

In addition to sharing technological capabilities, the partnership will allow Ant Financial and SPD Bank to strengthen collaboration on a broad range of inclusive finance initiatives, from improving user experience while using online and offline payment services, to providing secure, convenient and efficient financial services for small and micro businesses.

Last year at the 2017 Ant Fortune Open Platform Conference, Mr. Jing indicated that Ant’s technologies would be opened up to current and potential partners, with the only criterion being whether the partnership is innovative enough to deliver value to users.

In other words, Ant Financial is powering not only the biggest financial inclusion players worldwide like PayTM but also the biggest banks in the world, the big Chinese banks. Their open marketplace of apps, APIs and analytics are open to any other players, and the only criterion is whether the partnership is innovative enough to deliver value to users. I love this vision and approach and it is global, not local. Take note.

Chris M Skinner

Chris Skinner is best known as an independent commentator on the financial markets through his blog, TheFinanser.com, as author of the bestselling book Digital Bank, and Chair of the European networking forum the Financial Services Club. He has been voted one of the most influential people in banking by The Financial Brand (as well as one of the best blogs), a FinTech Titan (Next Bank), one of the Fintech Leaders you need to follow (City AM, Deluxe and Jax Finance), as well as one of the Top 40 most influential people in financial technology by the Wall Street Journal's Financial News. To learn more click here...