I’ve been blogging about digital transformation and one commentator asked me to qualify what I actually meant by a bank ‘transforming’ versus the others. This is something I intended to blog about but Bill Streeter over at The Financial Brand beat me to it in his reporting of research by BDO, the American assurance, tax, and financial advisory service.

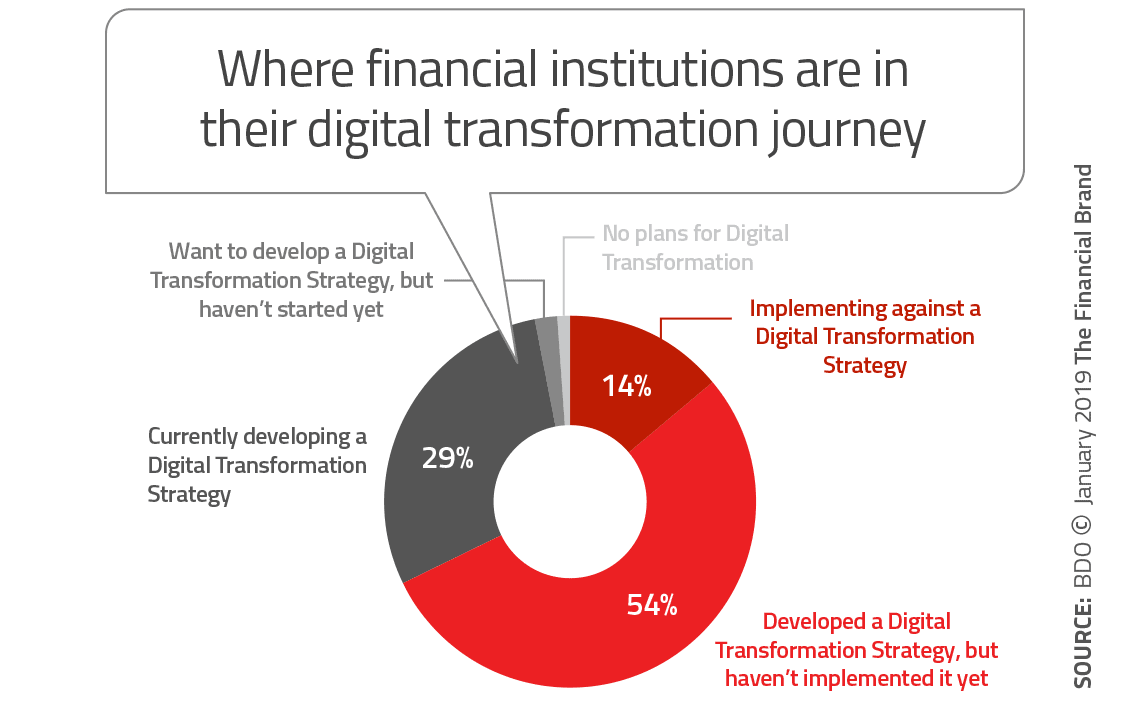

According to BDO, 14% of financial institutions are implementing digital transformation.

That surprises me as, of the 30,000 or so banks around the world, I can probably only point to less than ten that are truly transforming. Even so, with that caveat, I liked the way in which BDO defined transformation. They call it the “Innovation Maturity Scale”, which starts with:

- Business as Usual — No digital transformation initiatives

- Lab Rat —Try, test explore

- Opportunist — Placing smart bets and focusing on low-hanging fruit

- Strategist — Adapting; taking intentional steps toward a clearly defined strategy

- DNA — Culture of innovation, intrinsic to everything the institution does.

This maps quite closely to FinTech market evolution from a banks’ perspective, starting with banks that are just watching the FinTechs, to those that are working with them either by investing or partnering, to those that are truly mentoring and integrating FinTech into their DNA.

For me, it is the key qualifier however of when a bank truly gets digital and has it as part of the fabric of the firm. There really are not many that behave this way. They are few and far between, and the ones that do get this see technology as equally to finance in their operations. As I wrote recently, the Fin and the Tech are not separated but integrated. They are a FinTech bank, and there aren’t many of them.

The other useful part of the BDO study is their assessment of how digitally ready you are, as a bank. This is based upon three key factors:

- Business model maturity – creating new value, market differentiation and revenue in the digital economy

- Process maturity – operational reinvention by optimizing end-to-end process performance and improving efficiency.

- IT maturity – addressing or removing the IT complexities, risks and barriers to innovation.

All in all, a useful piece of work and if you’re wondering what or how to define your progress towards digitalisation, take the test. Is digital in the DNA of the bank? Does the leadership team drive digital transformation change or are they just investing in digital projects? How seriously is the bank stepping up to the challenge to convert from analogue? Are you really there culturally, organisationally, structurally, or is it just lip service?

That’s the difference between digital transformation and digital talk.

Chris M Skinner

Chris Skinner is best known as an independent commentator on the financial markets through his blog, TheFinanser.com, as author of the bestselling book Digital Bank, and Chair of the European networking forum the Financial Services Club. He has been voted one of the most influential people in banking by The Financial Brand (as well as one of the best blogs), a FinTech Titan (Next Bank), one of the Fintech Leaders you need to follow (City AM, Deluxe and Jax Finance), as well as one of the Top 40 most influential people in financial technology by the Wall Street Journal's Financial News. To learn more click here...