Building on my blog post last week, showing the views of 1997, it was clear years ago that banking was under siege. However, that siege never happened. Tesco thought that most banks were “a bunch of clowns”, but never cracked the market and still have not. Sainsbury may have onboarded customers, but they never built a sizable share. Wal*Mart tried for a decade to break into banking and failed. The mainstream banks in most markets have grown market share in the past quarter century. It hasn’t gone down a jot.

In fact, it amuses me to see all the talk about Amazon and Google going into banking as the same view was doing the rounds back in 1997 about Microsoft.

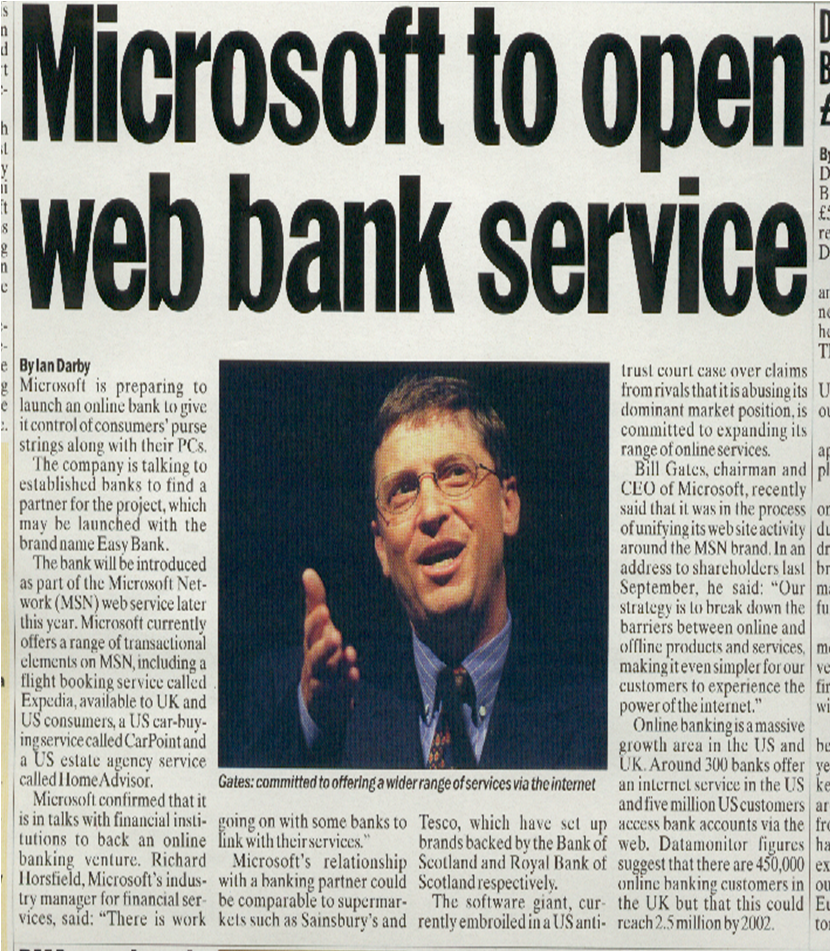

Bill Gates responded in January 1997, by saying:

“Microsoft will not apply for a banking licence, or become a bank, or do banking type functions. We are a technology provider. We are not interested in going into banking. Our expertise is software and helping banks in the banking business.”

I think the same applies to Amazon and Google and brethren.

However, there has been a fundamental shift in banking structure. Branches have closed in developed economies and will soon become a thing of the past. Mobile banking is where the action is and that forecast of 1997 that telecoms would become a major force in banking has come true. For example, I made this film twenty years ago …

… and still think that this integration of telecommunications, technology and finance that we now call FinTech was and is inevitable. Maybe that was influenced by my earlier work in NCR which, at the time, was part of AT&T. AT&T made a series of US commercials back in 1993/4, and these may have been part of what made me believe telco’s would merge with banks.

Some would say that the integration of telecommunications and finance has not happened. Others would say that this has not happened, but the integration of technology and finance has. I would argue that the move to the mobile network for financial services through Open Banking, Apps and Analytics is clearly restructuring the industry and providing opportunity for internet giants and start-ups but, more importantly, don’t underestimate the telco firms.

I guess it’s that old ‘boy who cried wolf’ thing, but it just seems obvious to me that the telco providers are upscaling from simple text payments to basic banking services. Orange has gone a step further and opened up a bank, but most bankers believe this is just noise and not serious.

Maybe so – Orange Bank has only got half a million customers in France and is now moving into Spain, so it’s no Revolut – but things are getting interesting. The neobanks like Revolut are gaining a million customers a month and FinTech specialist firms like Stripe were valued at $35 billion in September, which makes them more valuable than seven Manchester City’s, the world’s most valuable football club (that’s just in there for David Birch btw).

So, our view of the world is dominated by a few innovative start-up firms and the Big Tech giant fears. But what if an Orange acquired Commerzbank tomorrow, or a Vodafone merged with a Deutsche Bank? Is that a ridiculous idea?

I don’t think so, as they have the power, capital and customer base to do this. In addition, there’s a fundamental shift taking place, which is the telco industry upscaling finance from basic services to full service. Some people tell me that the telco folks don’t get banking. They don’t understand bps and what bankers mean by margin. Their focus is just more volume on the network. More services, more apps, more data.

However, one thing aligns telco firms with banks more than anything else, and that’s high touch frequent contact with the user. In fact, that’s the reason why we fear the Big Tech giants, but should we fear the telco giants more? Twenty years from now, if a Vodafone did buy a Deutsche Bank, what would the world look like?

Just a thought.

Chris M Skinner

Chris Skinner is best known as an independent commentator on the financial markets through his blog, TheFinanser.com, as author of the bestselling book Digital Bank, and Chair of the European networking forum the Financial Services Club. He has been voted one of the most influential people in banking by The Financial Brand (as well as one of the best blogs), a FinTech Titan (Next Bank), one of the Fintech Leaders you need to follow (City AM, Deluxe and Jax Finance), as well as one of the Top 40 most influential people in financial technology by the Wall Street Journal's Financial News. To learn more click here...