Living in a digital world, it’s hard to imagine being disconnected. Yet, some people are. According to a recent survey by Which? Magazine, four percent of consumers don’t have a mobile phone. Personally, I cannot imagine living without a mobile phone, but some people are happy to be off the network.

However, there’s an issue with this. If you’re off the network, you’re off the world.

This struck home to me in reading a consumer’s letter to a UK newspaper:

It is getting very difficult to carry out financial transactions online because I do not carry a mobile phone … banks insist on texting an authentication code and offering no alternative, other than going into the nearest branch. This presents another difficulty because where I live there are no branches left.

It’s something that us technofans cannot imagine: no mobile and having to go to a branch? It’s something that the technophobes fear: having a mobile.

It’s also something that the FinTech pundits probably don’t get: there are people out there who don’t want to bank online. A few years ago, the British Bankers Association (BBA) issued figures that showed two-thirds of UK consumers don’t use mobile banking and a third don’t use online banking, because they worry about security.

Even in 2020, half of consumers don’t use mobile banking and a quarter don’t use online banking. From The Guardian:

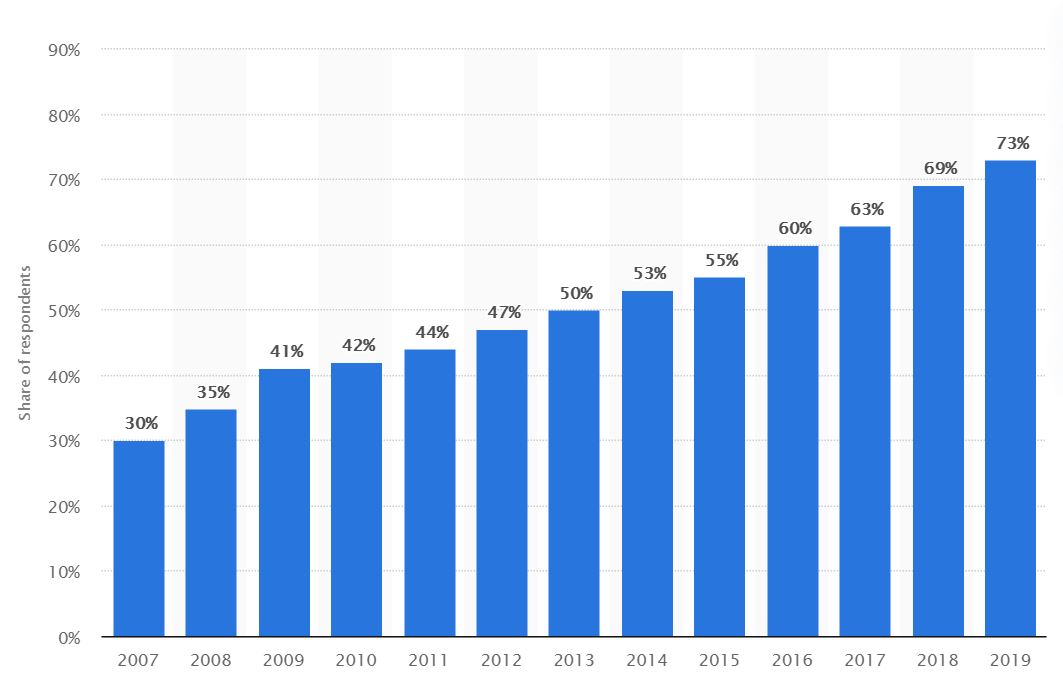

Over two-thirds of British adults used online banking and 48% used mobile banking in 2018 – up from 41% in the previous year, according to figures by UK Finance, the banking industry lobby group.

Source: Statista

Seventy-one percent of customers are expected to use mobile apps for banking by 2024. Over the same period, the number of customers who bank in branches is expected to decline to 55%.

The rapid uptake of app banking has forced Britain’s biggest banks to reassess their costly footprint of physical branches.

Britain’s banks have closed two-thirds of their branches over the last 30 years, according to Which?. There were more than 20,500 branches in the UK in 1988, but just 7,586 at the end of last year.

The reason for highlighting this is that my focus is on digitalisation of everything, automate everything, program everything. Let software eat the world. However, I do recognise there’s an issue here: What happens to those people who don’t want digital?

Digital automation makes sense for banking business as they can get rid of all physical overheads. Close branches, lay off humans, reduce costs, improve income. That’s the banking mantra, and it works.

My own mantra is slightly different. Improve service, enhance engagement, augment experience, exceed expectations. My own mantra is all about focus on the customer.

However, in all of this, what happens to the customer who doesn’t want this? What happens to the customer who like branches, enjoys physical engagement, likes the face-to-face experience and has an expectation of talking to a human?

Personally, I think that small group of people – currently just under a quarter of consumers – will be served by niche community banks and possibly large banks who strategically believe a direct engagement is still a critical part of their distribution structure. The latter are becoming less and less, so the former is where the focus lies.

In other words, being a small community bank with a direct engagement is not a bad thing. In fact, long-term, it may be the main thing for those banks. Just saying …

Postscript:

A survey conducted by fintech security provider Entersekt has found that over a third of British consumers (34 percent) distrust digital communications from banks to such an extent that they ignore actions the messages suggest they take.

The survey focused on consumers’ attitudes to “paperless banking” – the means by which banks and their customers communicate and administer accounts rather than the tools they use to transact. Conducted online by YouGov in March 2020, almost 2,300 consumers were polled on their experience of banking-related digital communications like emails, text messages, and banking portal notifications.

Results revealed a stark divide in the way different age groups perceive and respond to banks’ electronic messages. While 43 percent of respondents in the 55+ demographic said they “do not trust” digital communications, only 20 percent of 18–24-year-olds felt the same way.

What are older consumers worried about when it comes to digital communications? The survey provides some answers. A third of 55+ year-olds (33 percent) think they are “more likely” to fall victim to fraud through using digital channels. Only a fifth of 18–24-year-olds (20 percent) think the same way.

Chris M Skinner

Chris Skinner is best known as an independent commentator on the financial markets through his blog, TheFinanser.com, as author of the bestselling book Digital Bank, and Chair of the European networking forum the Financial Services Club. He has been voted one of the most influential people in banking by The Financial Brand (as well as one of the best blogs), a FinTech Titan (Next Bank), one of the Fintech Leaders you need to follow (City AM, Deluxe and Jax Finance), as well as one of the Top 40 most influential people in financial technology by the Wall Street Journal's Financial News. To learn more click here...