During this health crisis, everything has changed a lot. We are at home, home schooling, home learning, home entertaining, home working and more. Great. That’s all good. Yes and no. Mental health has become a big issue and is something everyone is talking about more as, after all, if you say at home for days, weeks and months on end, do you feel OK? I know that’s an issue but don’t want to go there right now. Instead, let’s talk about payments.

Yes, yes, I know, I’m boring. I always want to bring it back to money and finance and banking and technology. Well, right now, that’s not so boring. Right now, that’s one of the most exciting spaces to be.

After all, think about it. Since you were forced to stay at home, how has your financial behaviour changed? Did you download your bank’s app? Did you open a new digital bank account? Did you apply for a new payments card? Did you do things different?

According to various research, most of you did.

Amazon saw a rise in revenues of 40% in the second quarter of 2020, particularly in its cloud and retail services. Meantime, WH Smith saw its sales fall 85% year-on-year in April 2020.

In other words, we are seeing a K-curve crisis where digital firms are rising on the K-curve whilst physical firms whither on the vine or, rather, whither on the downside of the K.

It is as clear as that. In a lockdown climate, the K represents digital and physical. Digital is on the rise; physical is on the demise. The latter is clearly demonstrated by bars, restaurants, shopping malls, cinemas, airlines and more. No one wants to be near anyone else, for the moment at least.

What this means is that all behaviours have changed but, particularly, financial behaviours. We are ordering everything from home: our shopping, our services, our entertainment, our education, everything.

Digital firms are exploding because of this behavioural change but what does it mean for payment services?

From a retail consumer perspective, it meant that firms which are geared up for online digital checkout have prospered, as mentioned. But what does ‘geared up for online digital checkout mean?

It means that companies which were already focused upon mobile orders via apps and internet services with one click have done really well. Companies who had confusing checkout services, on mobile or online, have suffered. This sounds simple but it’s not so simple. In fact, it is why several multibillion dollar companies have been spawned in the last decade from Adyen to Square to Stripe, alongside several more specialised firms such as Curve, Currencycloud, Starling and TransferWise.

All of these companies are working in a new ecosystem where the internet enables apps, APIs and analytics to create smoother, easier and friction free commerce. Barriers in technology are coming down digitally, and at breakneck speed.

Some are adopting entirely new behaviours, e.g., baby boomers are pivoting to shopping online for groceries for the first time. Others are embracing online tools and software, like Google hangouts or Zoom, to expedite home-working (and the rest).

As the coronavirus touches pretty much every aspect of our lives, a need for friction-free immersion in all our digital touchpoints has become essential.

I like that term friction-free commerce. Maybe I should trademark it or, as my original entry before spell-checker stepped in, trademarket it!

One of my favourite examples for promoting friction-free commerce is Curve. It’s a start-up I’ve watched for a while which allows you to easily move between debit and credit cards as you checkout. Curve saw the need for friction-free finance years ago and, like others, is trying to break banking apart, repackage and rebundle it. Imagine the Netflix or Spotify of banking. Rebundling: it’s a greenfield area for finance. Swipe, view, send, spend and save. We’re going to want a friction-free balancing act between different accounts. Stateside, it fascinates me that most Americans have switched to using debit cards.

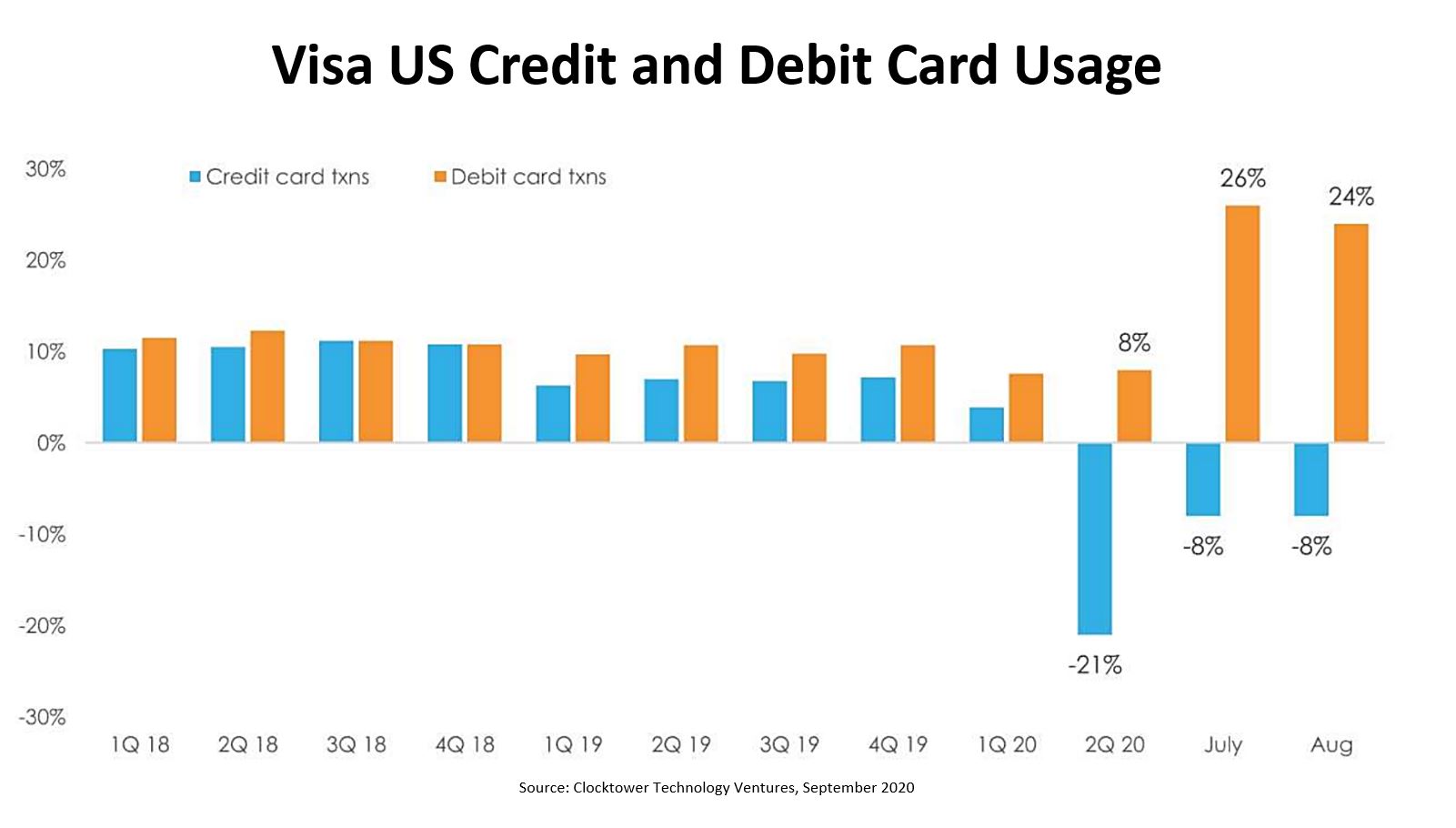

According to this report by Clocktower Technology Ventures, American consumers have shifted dramatically away from credit to debit card usage during this pandemic. More than this, it shifted to contactless debit card usage. This doesn’t surprise me. People, during a pandemic, move towards holding cash and avoiding debt. That’s a core reason why debit cards versus credit cards shifted, as people are scared of debt, especially at a time where they may never be able to pay it back.

In the world of issuers and acquirers, banks and providers, these are important changes as it is all about choice. The consumer wants more control over their finances and more choice. As a result, companies issuing cards need to be more aware of companies like Curve who can rebundle and repackage services to provide that choice. Equally and similarly it is why we need to focus upon how to rethink our world for 2021. Given our hunger for convenience and simplicity, the major shifts in ecommerce are probably going to take root in 2021.

The world of 2020 is all about digital. It’s all about digital choice, digital reach, digital services and digital payments. The more we can enable digital finance and payments easily and simply in friction-free commerce, the better. What are you doing to enable friction-free commerce?

Chris M Skinner

Chris Skinner is best known as an independent commentator on the financial markets through his blog, TheFinanser.com, as author of the bestselling book Digital Bank, and Chair of the European networking forum the Financial Services Club. He has been voted one of the most influential people in banking by The Financial Brand (as well as one of the best blogs), a FinTech Titan (Next Bank), one of the Fintech Leaders you need to follow (City AM, Deluxe and Jax Finance), as well as one of the Top 40 most influential people in financial technology by the Wall Street Journal's Financial News. To learn more click here...