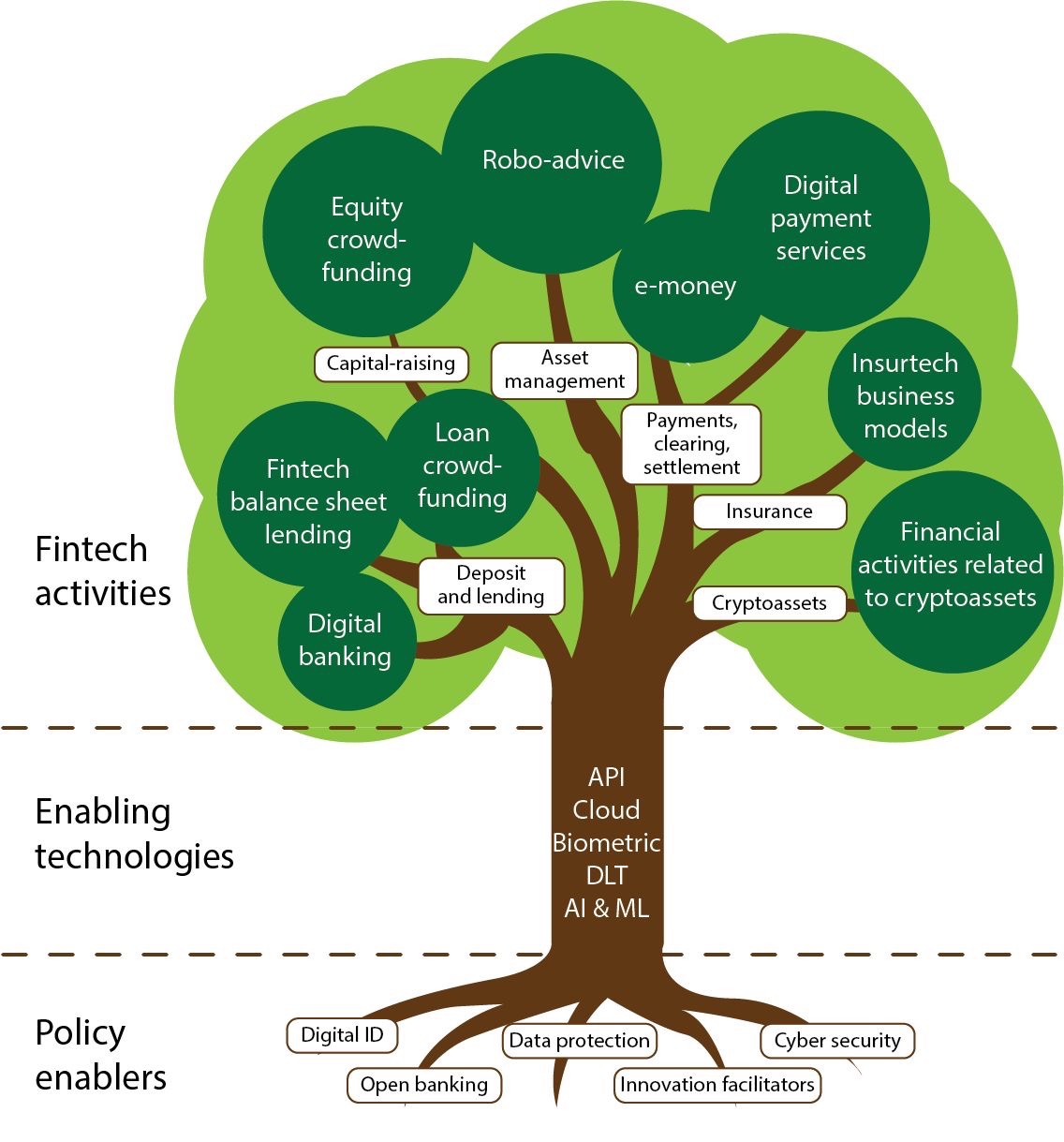

Jason Butcher, CEO of CoinPayments, posted this picture on LinkedIn the other day:

I like it.

The roots of innovation are in policies. The core of innovation is in the tree trunk’s technologies. The product of innovation is from enabling policies and technologies. True.

Except it doesn’t work that way.

The way it really works is sporadic and unpredictable; it is not planned or managed. Start-ups see emerging technologies that are enabling and start building upon them. The result is that the regulatory policies emerge far later than the technologies or innovations. Regulators are always in catch-up mode and rarely in enablement mode.

Luckily, in the past decade, this has changed. Having been around the block long enough, I’ve seen how regulations and regulators have developed. From the 1990s and 2000s, most regulatory activity was all about trying to control the miscreants of finance. Back then, by way of example, I worked closely with the EU policymakers and produced two regulatory books (about SEPA and MiFID). Back then, I was a boring old banking observer, and knee-deep in regulatory wrangles. I always remember one Eurocrat saying to me that the Payment Services Directive was not trying to create a single Eurozone at that stage but purely about getting all of the sheep in the pen. I asked him to clarify, and he continued the analogy.

We are the sheepdogs and the bank are the sheep. Our job is first of all to get all the sheep in the pen. Once we have achieved that, we then have the job to get all the sheep to face the same direction. Once we have achieved that, we then have to get all the sheep through the pen to the sheep shearer. Once we have achieved that, we have to shear the sheep and get them fit to leave the pen. That is what we do as regulators. We get the banks into the pen; we then get them to harmonize; we then clip their wings to suit the market; we then release them back into the markets.

Or something like that.

I liked this view a lot, as it rang true. Regulators in the 2000s were all about trying to get badly behaving banks to behave better but then, at the end of the 2000s, enabling technologies appeared – in particular cloud and the smartphone – and allowed a burgeoning group of FinTech start-up innovators to launch. The regulators were not prepared for this, but they liked the look of it as it would create more competition in finance. So, they enabled it.

Light licensing, particularly for payments processing, allowed the likes of Klarna and Adyen to flourish. The UK, particularly London, encouraged these innovations and led to the creation of the FinTech community that now leads the world. And regulators started innovation projects internally and sandboxes.

So much has changed in regulators over the past decade that it is almost unbelievable. Instead of clipping wings and getting sheep in the pen, today it is all about opening markets and enabling innovation yet, even then, there are issues arising. You open markets and enable innovation, and then some of the innovators throw mud in your face. Some, like Wonga, create bad market practices; others, like Powa, act like idiots; a few, like Klarna, emerge with questions about their business models; and finally there a small number of stand-outs, like Starling, who seem to have their act together and fit the new world of finance and tech, or FinTech as we prefer to call it.

From a regulators and regulatory viewpoint, the challenge is keeping up, protecting consumers, making sure things work right and avoiding failures. This does not mean that regulators have to be completely risk-averse as, in the past decade, they clearly are not; but it does mean that regulators have to try to be more future-focused than looking in the rear-view mirror. For most of my time working with banks, regulators were looking backwards; thank goodness, in the last decade, they are looking forward.

Meantime, if I redrew Jason’s tree, the roots are in technology; the trunk is in new business models and ideas; and the leaves are the enabling policies that enable those leaves to flower.

Chris M Skinner

Chris Skinner is best known as an independent commentator on the financial markets through his blog, TheFinanser.com, as author of the bestselling book Digital Bank, and Chair of the European networking forum the Financial Services Club. He has been voted one of the most influential people in banking by The Financial Brand (as well as one of the best blogs), a FinTech Titan (Next Bank), one of the Fintech Leaders you need to follow (City AM, Deluxe and Jax Finance), as well as one of the Top 40 most influential people in financial technology by the Wall Street Journal's Financial News. To learn more click here...