The key thrust of my new book is the intelligence revolution.

More on that tomorrow but the basics are that we are living through the third technology revolution of finance and banking. The first began with automating the mundane with mainframes from the 1950s onwards (back office efficiencies fifty years ago); moving to making the customer digitally connected through cloud and mobile (the front experience in the 2010s); and are now moving to being AI-natively brilliant by allowing digital agents to do everything for us (connecting back and front office tasks in the 2020s).

Each of these are fundamental changes.

The first demanded the implenetation of basic connections that involved high cost capital-intesive projects that took years; the seoncd focused upon opening banking and financial processes, and gave opoorunty for many digital providers to enter the markets or, in other words, the fintech revolution of neobanks, challenger banks and more; and now the third is focused upon moving from being digital-native to AI-native, where everything in every part of the organsation is maximised for interactivity, support, risk, compliance and, most of all, customer cushion.

What do I mean by a ‘customer cushion’?

I mean that every part of connecting with customers is intelligent. This means that customers are never going to have to think about banking ever again, because the bank thinks for them. The bank does everything on their behalf intellignelty through agents and bot-to-bot commerce. All you need to do is swipe left or right when asked. That’s it.

What I loved about the Huawei meeting in Shanghai last week is that they agree with everything I say (I’m selfish that way), but was surprised to see some of the slides of their financial markets leader, Jason Cao, that are so aligned and close to my way of thinking that it was like he was sharing my book on stage.

Let’s have a quick look by checking out a few of Jason’s slides.

The first I noted is how Huawei has developed their financial vision over the past 16 years from being IP focused to AI-native.

For the 2010s, I was banging on and on about legacy transformation to digital at the core. The slide shows the same. Now, we are talking about being AI-native with intelligence at the core. That’s the revolution now.

As I’ve said quite often, if you are still doing digital, you are too late.

Jason then presented a slide about moving from the digital to the real-time economy.

The real-time economy demands real-time reactions and interactions. Why am I sitting on a phone call saying your call is important to us … you are fifteenth in the queue and get answered after 90 minutes when I could talk to a real-time, AI-drivien, human avatar who is actually more personal, more interactive and more real than any human call centre agent?

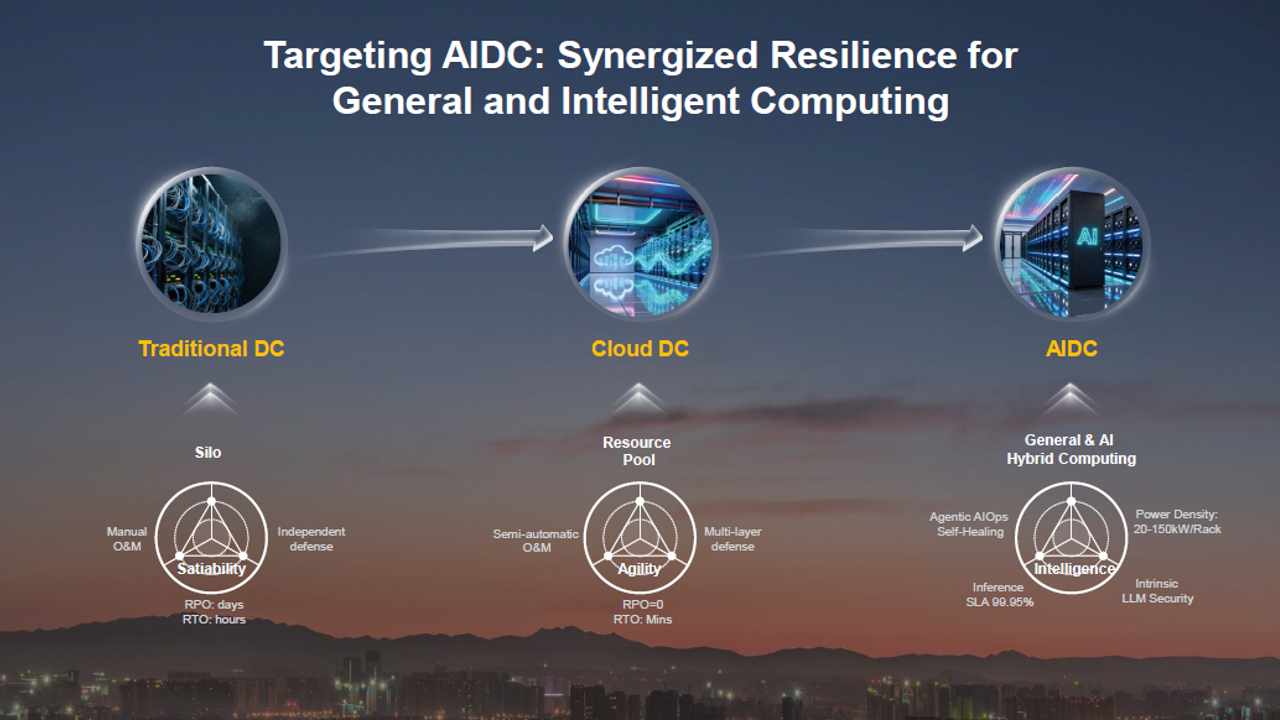

Then there’s this slide:

We have the old automating the mundane with mainframes that were silo-based, transaction-focused and pretty dumb.

The movement was then to digitalise.

Digital created agility through cloud, APIs, opening up finance to deliver services that improved every transaction and interaction. It should have been done by now because we are now moving one step beyond. The AI data centre, or AIDC.

AI is fast, real-time, remembering, and integrates the power of knowledge into open banking, API systems we built in the last decade.

I could add so much more, but you get the message: first tech revolution was about efficiency; the second was about the customer experience; and the third is all about knowledge to manage risk, compliance, fraud and, most of all, the customer cushion.

At the heart of the customer cushion is trust. Can I trust you are who you say you are? Can I trust the data?

These are core themes of Intelligent Bank, although there’s a fourth revolution coming soon. Can you guess what it is yet?

Chris M Skinner

Chris Skinner is best known as an independent commentator on the financial markets through his blog, TheFinanser.com, as author of the bestselling book Digital Bank, and Chair of the European networking forum the Financial Services Club. He has been voted one of the most influential people in banking by The Financial Brand (as well as one of the best blogs), a FinTech Titan (Next Bank), one of the Fintech Leaders you need to follow (City AM, Deluxe and Jax Finance), as well as one of the Top 40 most influential people in financial technology by the Wall Street Journal's Financial News. To learn more click here...