The latest McKinsey Global Banking Annual Review paints a fascinating picture of modern banking and shows that the industry is both richer than ever and more threatened than ever.

On the surface, everything looks fantastic. Global banking generated around $1.3 trillion in net income in 2025, making it one of the most profitable industries on Earth. Revenues, deposits and assets all continued to grow, and many banks benefited from higher rates, stronger balance sheets and years of post-crisis restructuring.

But McKinsey’s core argument is that these numbers are disguising a deeper structural problem. Banks are making record profits whilst simultaneously losing strategic relevance.

The old model of banking was based upon ownership of the customer relationship. Customers kept deposits with one institution, borrowed from the same institution, invested through the same institution and generally stayed loyal because moving money was inconvenient and slow. That “stickiness” created enormous profitability.

McKinsey argues that this stickiness is now dissolving.

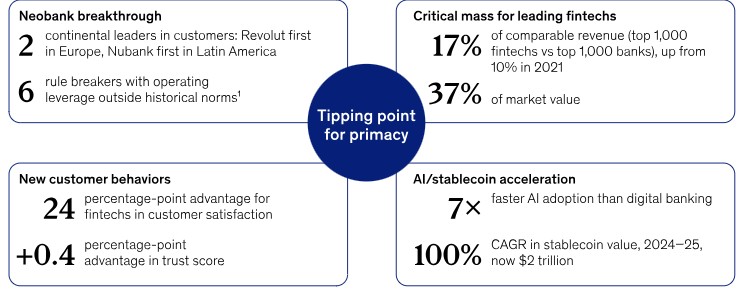

First came fintechs. For years, incumbents treated fintech startups as irritating but small challengers. Now companies such as Revolut and Nubank have reached meaningful scale, profitability and trust. According to the report, the largest fintechs now account for roughly 17% of combined banking and fintech revenues, growing far faster than traditional banks.

Then comes the next wave: agentic AI and digital assets.

This is where the report becomes really interesting. McKinsey believes AI is not simply another efficiency tool. It changes the economics of customer ownership itself.

For decades, banks relied on customer inertia. Most consumers did not optimise savings rates, refinance debt regularly or constantly move money between providers because it was too much effort. AI agents remove that friction. Intelligent systems can automatically search for better rates, switch providers, optimise deposits, manage liquidity and compare products continuously in real time. In other words, AI turns banking into a constantly competitive marketplace rather than a relationship business.

That is a profound shift.

The report also highlights how quickly this transformation is happening. Previous technological revolutions — internet banking, smartphones, apps — took years or even decades to penetrate older demographics. AI adoption is happening across all age groups almost simultaneously. McKinsey notes that there is effectively no “grace period” this time.

This fits perfectly with what many of us are already seeing. The digital revolution was about moving from physical banking to online banking. The intelligence revolution is about moving from humans navigating systems to systems navigating finance autonomously on behalf of humans.

The other major theme is geography. McKinsey argues that banking is fragmenting into distinct regional models rather than converging into one universal global model. Asia, Africa and parts of the developing world may leapfrog legacy Western banking structures entirely because they are building AI-native and digital-native infrastructures from scratch.

That is particularly important because many Western banks remain trapped by legacy technology. They still run fragmented architectures, siloed data and decades-old operating models. McKinsey repeatedly stresses that AI only works when supported by clean, integrated, machine-readable data. Or put more bluntly: you cannot build intelligent banking on dumb infrastructure.

The report’s answer is what McKinsey calls “precision with speed”. Banks can no longer survive through sheer scale or balance-sheet heft alone. They need hyper-personalised customer engagement, AI-driven decisioning, rapid experimentation and platform-based operating models. The future bank looks less like a giant bureaucracy and more like a network of intelligent services operating at multiple speeds simultaneously.

The irony is that banks have never been more profitable, yet many may never have been more vulnerable. The danger is not collapse. The danger is becoming invisible infrastructure underneath somebody else’s intelligent platform.

Meanwhile, in another report, McKinsey argues that the future of digital money is much bigger than stablecoins. While most media attention focuses on firms like Circle and Tether, the real transformation is happening inside the banking system itself, where tokenized deposits are already moving more than $4 trillion a year.

The report says we are moving towards a three-layer monetary architecture. At the top are stablecoins, which are best suited for fast-moving, lower-value transactions and cross-border payments. In the middle are tokenized bank deposits, where banks place traditional deposits onto blockchain rails while keeping them on their balance sheets. At the foundation sits central bank money, including future wholesale CBDCs, which provide the ultimate settlement layer and remove counterparty risk between institutions.

McKinsey argues that stablecoins have generated enormous excitement, but the actual scale remains relatively small compared with global finance. Stablecoin circulation is around $300 billion, and annual payment activity is still tiny compared with the trillions flowing through traditional banking systems every day. By contrast, major banks are already running large-scale tokenized deposit networks. JPMorgan’s Kinexys platform alone reportedly processes more than $1 trillion annually.

The key distinction is that stablecoins effectively move money away from bank deposits into third-party issuers, which can weaken banks’ funding models. Tokenized deposits do the opposite. They allow banks to modernise money using blockchain technology while keeping customer deposits, liquidity and relationships inside the banking system. In McKinsey’s view, this makes tokenized deposits far more attractive to large financial institutions.

The biggest challenge is interoperability. Today, most banks are building their own tokenized deposit systems, creating a collection of isolated networks. The next battle is therefore not technology but standards, legal frameworks and shared rulebooks. Projects such as BIS Project Agora, Swift’s orchestration initiatives, Partior and the Canton Network are all attempting to solve this problem by allowing different tokenized money systems to communicate with each other.

McKinsey’s broader conclusion is that the future of money will not be one dominant digital currency replacing everything else. Instead, it will resemble a layered financial stack. Stablecoins become the “money in motion” layer, tokenized deposits become the “money at rest” layer for institutional finance, and central bank money becomes the final settlement layer. The winners will be the institutions that can make these layers work together seamlessly.

In summary, the report is really saying this: everyone is talking about stablecoins, but the real revolution is that banks are quietly rebuilding the plumbing of money itself. Stablecoins may be the visible tip of the iceberg, but underneath, banks, central banks and payment networks are constructing an entirely new on-chain financial infrastructure that could eventually move trillions of dollars globally in real time.

Chris M Skinner

Chris Skinner is best known as an independent commentator on the financial markets through his blog, TheFinanser.com, as author of the bestselling book Digital Bank, and Chair of the European networking forum the Financial Services Club. He has been voted one of the most influential people in banking by The Financial Brand (as well as one of the best blogs), a FinTech Titan (Next Bank), one of the Fintech Leaders you need to follow (City AM, Deluxe and Jax Finance), as well as one of the Top 40 most influential people in financial technology by the Wall Street Journal's Financial News. To learn more click here...