I’ve recently seen so many articles about branches and

branch closures that it’s worth a blog post, just to keep up with the issue.

The first thing that came out was the recent European

Central Bank (ECB) data detailing bank statistics over the past few years.

From analysing this data, Reuters found that there has been significant branch closures, particularly in

austerity countries like Spain:

“Banks have shut about 20,000 branches across Europe in the

last four years, including 5,500 last year and 7,200 in 2011. That represents the closure of about 8% of

Europe's branches since the financial crisis, and the cull is expected to

continue for many years.”

“The cuts have been most severe in Spain, unravelling years

of expansion by regional savings banks, which had landed it with the biggest

network in Europe. Its branch numbers

were down 17% by the end of 2012 from four years earlier. But at just over

38,200 branches, Spain still had more branches per head than any country in

Europe - one for every 1,210 people.”

“France had the most branches in Europe by the end of last

year, with nearly 38,450, or one for every 1,709 people, behind only Spain and

Cyprus per person. Cyprus had one branch

per 1,265 people.”

France “shed less than 3% of its network in the four years

to the end of 2012, while 5% of UK branches and more than 8% of German ones

pulled down the shutters for the last time. The number of branches plummeted by

a third in Denmark and by a quarter in the Netherlands.”

British “banks have almost halved branch numbers since 1990.

Senior bankers privately say a network of 700-800 outlets would be an optimal

size for a bank covering all of Britain. None of the big five have so few.

Lloyds has three times that (2,260), and Royal Bank of Scotland more than twice

(1,750), excluding almost 1,000 branches they are already selling between them.”

British banks closed 557 branches over the last four years resulting

in 11,713 branches in 2012, compared with 12,270 in 2008. Between 2008 and 2011, HSBC closed 181

branches, NatWest 135 and Barclays 99.

The British Bankers Association (BBA) are about to produce a further update to these statistics which will show a

further 68 branches were closed by HSBC in 2012, 60 by RBS/NatWest in the first

half of 2013 and 30 by Barclays. HSBC has announced another 25 closures are anticipated,

as HSBC pushes more focus upon its partnership with Marks & Spencer and banking

through Post Offices.

The figures are more dramatic in the UK if you dig

deeper. According to a recent study by Nottingham

University,

nearly 7,500 branches closed between 1989 and 2012 which would account for 40%

of all branches in Britain.

The USA is the one country that has consistently refuted the

need to close branches, expanding the branch footprint from around 80,000 in

2000 to over 95,000 in 2012. Even there,

we are seeing a final day of reckoning with branches closures rising in the last twelve months.

From a recent article in St Louis Today: “Bank branches in the U.S. fell to 97,337 this year (2013), reflecting a loss of 867 branches in 2012, according to SNL Financial. From 2010 to 2011, branches nationally declined by about 315.”

The writing is on the wall, as illustrated by the

Motley Fool saying that bank branches are going the same way as bookshops and record

stores:

“With a 4% average annual decline in branch traffic over the

past 16 years, banking is the natural next domino to fall … the competition

among online banks, particularly from names like Ally Bank and ING and

Everbank, is likely to cut into margins — but Bank of Internet does have

admirably high Return on Equity (ROE) and a high earnings growth rate compared

to all of the more traditional banks I looked at (their ROE is around 16%, even

great banks like Wells Fargo are down around 13% and most are closer to 10% or

less, sometimes far less.”

I’ve written about this before ...

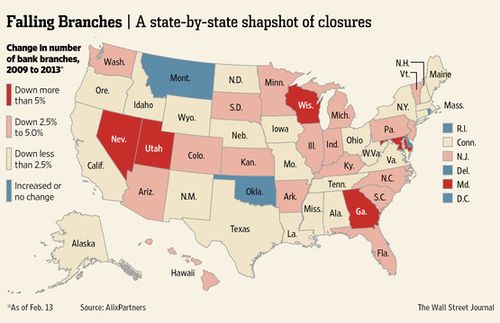

... and tend to agree with the research by AlixPartners, a New York consulting firm,

who are quoted in the Wall Street Journal as estimating that American banks will cull 1 in 5 branches over the next

decade, putting the total closer in line with 2000 levels.

Perhaps this is further illustrated in the same article by comments from PNC

Financial Services Group President, Wiulliam Demchak. The

Pittsburgh-based bank operates 2,900 branches and are closing 200 this year as the bank’s focus going

forward “will be weighted far more in the direction of technology than teller

lines”. Each time a PNC customer

deposits a check by snapping a picture on a mobile phone, that saves the bank

$3.88 per transaction compared with a deposit at a teller window.

There are other statistics worth noting in the

WSJ article,

such as:

- The number of U.S. branches doubled over the

past three decades, and the industry has reduced branches just three times in

the 77 years since the FDIC started keeping track

- Online banking now accounts for 53% of banking

transactions, compared with 14% for in-branch visits, according to research

from AlixPartners

All in all, the writing is clearly on the wall when you see

the statistic that the Top 30 American banks spend $50 billion a year on their

branches.

This is well illustrated by the Financial Times who state that:

- Bank of America has cut the number of its branches to 5,243

in the third quarter, a 6% decline from the same period last year

- Citigroup has reduced its branches aggressively over the

past seven consecutive quarters, reducing outlets to 3,777 from 4,069 a year

ago

So here’s the bottom-line: if you are not aggressively

looking to migrate customers from physical to digital distribution, then you’re

a dead bank (see Monty Python for more informed

opinion).

A customer enters a bank’s head office.

Mr. Praline: Hello, I wish to register a

complaint.

(The concierge does not respond.)

Mr. Praline: Hello, Miss?

Concierge: What do you mean “miss”?

Mr. Praline: (pause) I’m sorry, I have a

cold. I wish to make a complaint!

Concierge: We’re closing for lunch.

Mr. Praline: Never mind that, my lad. I wish to

complain about this bank branch what I invested in not half an hour ago from

this very bank.

Concierge: Oh yes, the, uh, the Northern Rock...What’s,uh...What’s

wrong with it?

Mr. Praline: I’ll tell you what’s wrong with it,

my lad. It’s dead, that’s what’s wrong with it!

Concierge: No, no, it’s uh,...it’s resting.

Mr. Praline: Look, matey, I know a dead bank

branch when I see one, and I’m looking at one right now.

Concierge: No no it’s not dead, it’s resting!

Remarkable bank, the Northern Rock, isn’t it, ay? Beautiful security!

Mr. Praline: The security doesn’t enter into it.

It’s stone dead.

Concierge: Nononono, no, no! It’s resting!

Mr. Praline: All right then, if it’s resting, I’ll

wake it up! (shouting at the branch) Hello, Mister Money Banks!

I’ve got a lovely fresh pensioner customer for you if you show...

(concierge hits the branch)

Concierge: There, it moved!

Mr. Praline: No, it didn’t, that was you hitting

the wall!

Concierge: I never!!

Mr. Praline: Yes, you did!

Concierge: I never, never did anything...

Mr. Praline: (yelling and hitting the branch

repeatedly) HELLO BANKER!!!!! Testing! Testing! Testing! Testing! This

is your nine o’clock alarm call!

(Takes branch and thumps it on the counter. Throws it up

in the air and watches it plummet to the floor.)

Mr. Praline: Now that’s what I call a dead bank

branch.

Concierge: No, no.....No, it’s stunned!

Mr. Praline: STUNNED?!?

Concierge: Yeah! You stunned it, just as it was

wakin’ up! Northern Rocks stun easily.

Mr. Praline: Um...now look...now look, mate, I’ve

definitely had enough of this. That bank branch is definitely deceased, and when

I purchased it not half an hour ago, you assured me that its total lack of

movement was due to it being tired after a prolonged financial crisis.

Concierge: Well, it’s probably pining for the old

days.

Chris M Skinner

Chris Skinner is best known as an independent commentator on the financial markets through his blog, TheFinanser.com, as author of the bestselling book Digital Bank, and Chair of the European networking forum the Financial Services Club. He has been voted one of the most influential people in banking by The Financial Brand (as well as one of the best blogs), a FinTech Titan (Next Bank), one of the Fintech Leaders you need to follow (City AM, Deluxe and Jax Finance), as well as one of the Top 40 most influential people in financial technology by the Wall Street Journal's Financial News. To learn more click here...