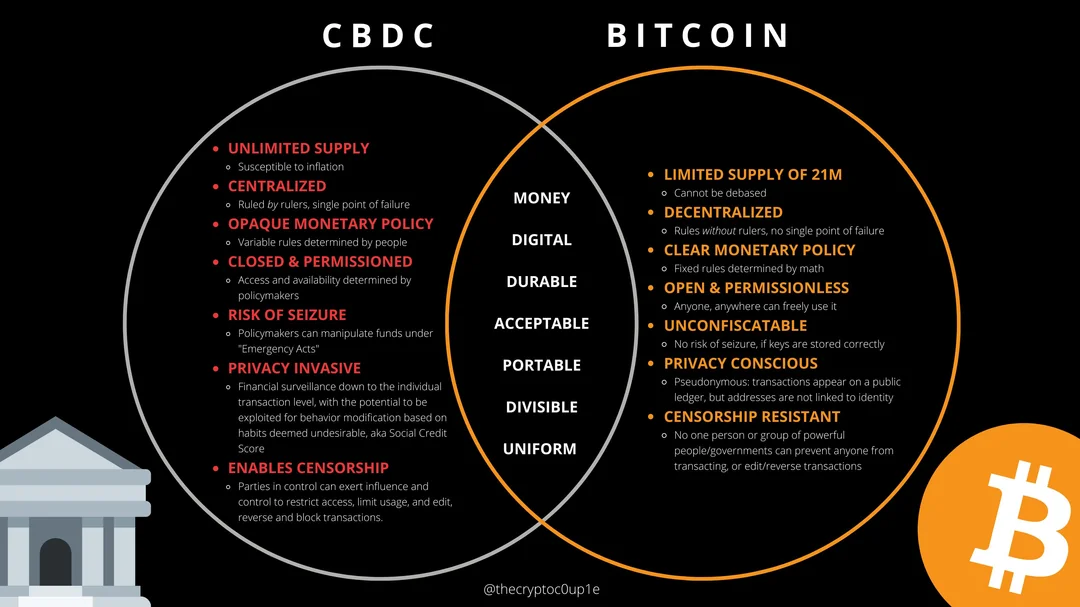

I’m discussing a lot about digital currencies these days, and the future of CBDCs, Stablecoins and Crypto. The conversation generally goes along the lines of central banks issuing digital currencies is really unnecessary. No one wants them and no one trusts them. The whole thing is just a scam for governments to track and trace you, and banks are concerned about how this might undermine their intermediation position. Generally, amongst banks, corporations and citizens, there is a lot of distrust of CBDCs*.

But equally, there’s a lot of distrust of cryptocurrency. For years, Jamie Dimon has been calling bitcoin a scam, and most cryptocurrency assets are blocked due to the view that it’s all being used for criminal activities. By way of example, I tried to move funds from Coinbase to Wise the other day and got this message: “Wise does not accept cryptocurrency payments, including those from Coinbase”.

It turns out that this is because, in their small print, this is unacceptable use of their platform which points out they will not accept fund movements from “companies involved in the exchange or trading of cryptocurrencies, or any other virtual currencies including payments for the purpose of purchasing cryptocurrencies.”

It is confusing however, as they also say that “you can receive money to your Wise account from a platform that deals with cryptocurrencies — as long as the platform is regulated and/or supervised in the EU or UK and is within Wise’s risk appetite and per Wise’s discretion”.

So why won’t they accept payouts from Coinbase when the banks do? Well it is because each institution has a different position and interpretation:

- HSBC: Restricts credit card purchases of crypto and imposes daily limits on debit card transactions.

- NatWest: Blocks transactions to and from major crypto exchanges and has introduced low daily limits on transfers.

- Santander: Similar to HSBC, Santander restricts credit card purchases and imposes daily limits on debit card transactions.

- Nationwide: Recently introduced daily limits for crypto purchases and restricts credit card transactions.

- Barclays: Allows transactions but monitors them closely for any suspicious activity.

- Starling Bank: Among the first to ban cryptocurrency purchases, blocking both debit card payments and bank transfers to buy or sell crypto.

- Revolut: One of the most crypto-friendly institutions, allowing users to buy, sell, and transfer cryptocurrencies freely.

Maybe this is why Revolut has experienced substantial customer growth, reaching 52.5 million customers globally by the end of 2024, a 38% increase. In the UK, their customer base hit 10 million, solidifying their position as a major player in the country's fintech sector. It is because they are delivering what the customer wants. That is why JPMorgan now deals in bitcoin, even though Jamie Dimon hates it.

In fact, it is clear that any bank will support digital assets if the customer wants it and the regulator allows it. For example, Lloyds Banking Group’s policy is that they will allow “deposits and withdrawals to and from regulated cryptocurrency exchanges like Coinbase”. Coinbase is a fully regulated crypto exchange under the regulator’s rules:

“Coinbase has received regulatory approval from the UK's Financial Conduct Authority (FCA) to operate as a Virtual Asset Service Provider (VASP). This approval allows Coinbase to offer a wider range of crypto and fiat services to customers in the UK.”

But then that was only in February 2025 and, at the speed of a snail, I am pretty sure the other institutions catch-up eventually, and yes, I am talking to you Wise.

Even as they do, there are still major concerns about crypto usage as regulators are clear that any bank that allows criminal or suspicious activities through crypto transactions will be severely punished. This is why most are scared of crypto usage and yet, on the other hand, you don’t need banks or fintechs to deal in crypto. You just do it person-to-person in a democratised network. Wasn’t that the original idea?

“A purely peer-to-peer version of electronic cash would allow online payments to be sent directly from one party to another without going through a financial institution.” Satoshi Nakamoto’s White Paper Bitcoin: A Peer-to-Peer Electronic Cash System, November 2008

Who needs banks and fintechs?

Well, most of us do because we have no idea how to deal in memecoins, cryptocurrencies and the complexity of unregulated exchange systems.

Which brings us to stablecoins, the middle ground between CBDCs and cryptocurrencies, and what appears to be the fastest growing area of trust. This is because stablecoins are tied to real world physical money – the dollar, euro and yuan – but can be used digitally with financial institutions as well as direct.

There has been a lot movement towards stablecoins in the past year or two. By way of example:

- Almost $30 trillion - $27.6 trillion in 2024 – is being transacted in stablecoins, which is more than Visa and Mastercard combined

- There are over 30 million stablecoin active wallets, up 53% year-on-year

- Worldpay pays creators, contractors, and sellers in stablecoins (USDC) with no wallets, custody and near instant settlement

- JPMorgan, Citi, Visa, PayPal, Circle and more are firmly building stablecoin rails and making such developments a firm favourite on Wall Street

Thanks to Robert Acres for these insights.

The Financial Times makes it clear that there is a gold rush going on here.

“Some of the world’s largest banks and fintechs are rushing to launch their own stablecoins … their enthusiasm has been fuelled by growing acceptance among regulators around the world that stablecoins, designed to hold a constant value of a dollar per coin, could become a more accepted part of the financial system.”

Making this clearer, in a letter responding to the FT’s article, Sveinn Valfells who is Co-founder and Chair of Monerium, writes:

“Stablecoins don’t just facilitate payments in emerging markets with poor infrastructure. According to Stripe, blockchain-based stablecoins ‘make money movement cheaper and faster’, and they are ‘globally available, open-access and programmable’. Moreover, stablecoins issued under European e-money regulations are fungible with cash, as evidenced, for example, by the fact that the ECB accounts for e-money in the same way as demand deposits. E-money is safeguarded under stringent, standard rules; it’s not the brand that tells you what the credit risk is, it’s the licence.”

The clear point here is that stablecoins are digital cash, and are becoming the preferred currency of banks, corporations and the world of money we live in today. This is because, if the world does not trust CBDCs and cryptocurrencies, they can trust stablecoins. This is why we are seeing a turbocharged boost to the next world of trusted digital value exchange.

* Central Bank Digital Currencies, just in case you’re not aware

Chris M Skinner

Chris Skinner is best known as an independent commentator on the financial markets through his blog, TheFinanser.com, as author of the bestselling book Digital Bank, and Chair of the European networking forum the Financial Services Club. He has been voted one of the most influential people in banking by The Financial Brand (as well as one of the best blogs), a FinTech Titan (Next Bank), one of the Fintech Leaders you need to follow (City AM, Deluxe and Jax Finance), as well as one of the Top 40 most influential people in financial technology by the Wall Street Journal's Financial News. To learn more click here...