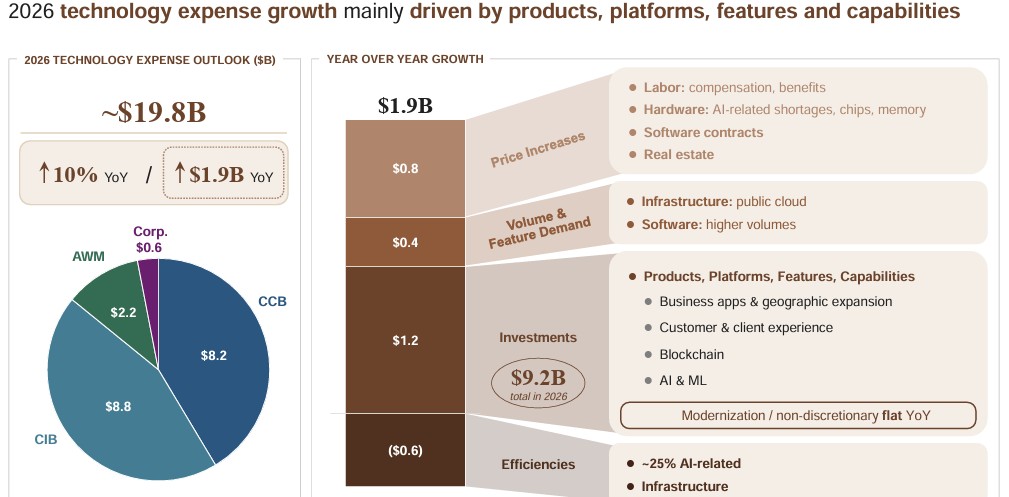

There’s been a lot of talk this week about JPMorgan spending $20 billion on technology in 2026.

It sounds huge, and it is, and it’s slightly more than their peer group spend but, bear in mind, this is a bank worth over $800 billion and with revenues of $185 billion, so you need to put this in perspective.

What does this $20 billion investment mean? My friends at PYMNTS.com explain:

- JPMorgan’s planned annual tech spend marks a shift from patchwork upgrades to full core transformation, rebuilding banking around cloud, data and AI-driven, real-time systems;

- Competitive advantage is moving from balance-sheet scale to software and proprietary data, enabling automated decisioning, embedded finance and platform-style banking model; and

- As large banks modernize, FinTech’s edge in speed and UX may shrink, pushing startups toward niche innovation, partnerships and infrastructure rather than end-to-end disruption.

Nasdaq notes that JPM’s technology strategy is now “a core, multi-year competitive investment rather than a discretionary cost lever”

CNBC’s Hugh Son, a long-term observer of JPMorgan’s strategy – he and I met a decade ago talking about the bank's AI strategy – sees a different angle noting that CEO Jamie Dimon described his bank’s internal plans is to shift employees into new roles. “We already have huge redeployment plans for [our] own people,” Dimon said. “We have displaced people from AI — and we offer them other jobs.” This is why the bank’s head count was roughly unchanged at 318,512 over the past year, but there were changes below the surface.

What I noted however is a subtext that the techies miss. They are opening lots of new branches. The Financial Times noted just the other day that JPMorgan are increasing their branch footprint significantly.

JPMorgan Chase aims to open more than 160 branches in more than 30 states in 2026, part of a multibillion-dollar investment into its brick-and-mortar network that reflects a broader bet by US banks on Americans’ enduring fondness for in-person banking.

In other words, there are two things in play here: physical and digital. Digital self-service for everyday banking; physical service for those who need more.

“We know that building branches and getting into markets is a critical part of getting … deposit share,” said Jennifer Roberts, chief executive of Chase consumer banking.

The FT reports that their aim is for newly opened branches to be profitable within four years, and is achieving that goal “months” faster than planned thanks to growth in deposits, card customers and wealth management clients at the retail locations.

I am in a debate with a friend about what to call this, as I do not like the term phygital. It sounds like you have ants in your pants. My preferred term is O2O - online to offline - as it resonates with H2O, which is essnetial for us to live and exist. What do you think?

Anyways, here is the whole report and, along with comments above, I was particularly impressed by the bank’s dashboard on page 20.

Enjoy.

Chris M Skinner

Chris Skinner is best known as an independent commentator on the financial markets through his blog, TheFinanser.com, as author of the bestselling book Digital Bank, and Chair of the European networking forum the Financial Services Club. He has been voted one of the most influential people in banking by The Financial Brand (as well as one of the best blogs), a FinTech Titan (Next Bank), one of the Fintech Leaders you need to follow (City AM, Deluxe and Jax Finance), as well as one of the Top 40 most influential people in financial technology by the Wall Street Journal's Financial News. To learn more click here...