The next era of payments: when money moves at internet speed

I just found an interesting report by KPMG about a new payment standard called x402. Have you heard of it? If you haven’t, it’s built to ensure open, free, frictionless payments, and could be revolutionary for embedded, invisible finance.

Built by Coinbase, the x402 protocol is an open-source, web-native payment standard.

It was launched in May 2025 to enable AI agents, APIs, and content using stablecoins (primarily USDC) to pay for services, and key partners supporting this infrastructure include Cloudflare, Circle, Stripe, and AWS.

Why is it called x402? Because it acts as an HTTP for money, using the long-unused 402 HTTP status code, for automated machine-to-machine or human-to-machine transactions.

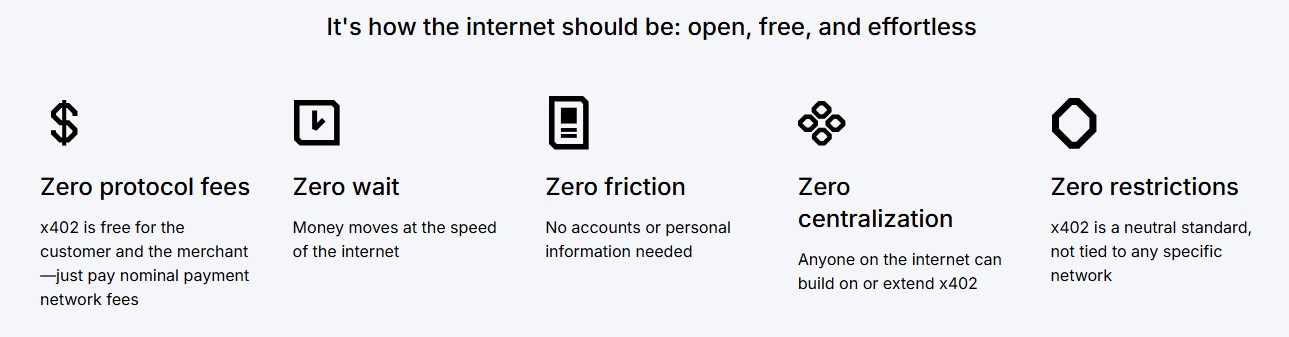

TBH, it aims to solve an issue that’s been around for the past fifty years. What’s the issue? The fact that the internet was never designed for commerce. It was designed for information exchange.

For most of the past fifty years, payments have been built on infrastructure designed for a different world: a human-centric, card-based, offline financial system. Yet today’s economy is digital, always-on, and increasingly autonomous. The result is a growing mismatch between how the internet works and how money moves.

The past decade has delivered extraordinary progress – instant payments, open banking, digital wallets and stablecoins – but the core rails still reflect legacy design principles. Cross-border payments still pause for weekends and holidays, onboarding still requires accounts and credentials, and transactions still assume a human at the keyboard … but the next phase of the digital economy won’t be driven primarily by humans … it will be driven by machines.

So x402 addresses a key flaw in today’s internet: native payments.

For decades, the internet has lacked a native way to transfer value. We built the web to exchange information, not money. As a result, the industry created workarounds – subscriptions, paywalls, stored cards and billing systems – all of which introduce friction and inefficiency.

Now a new approach is emerging.

x402 proposes an internet-native payment standard that allows systems to request and receive payment directly through standard web interactions. In simple terms, it makes payments as easy as sending a web request or email.

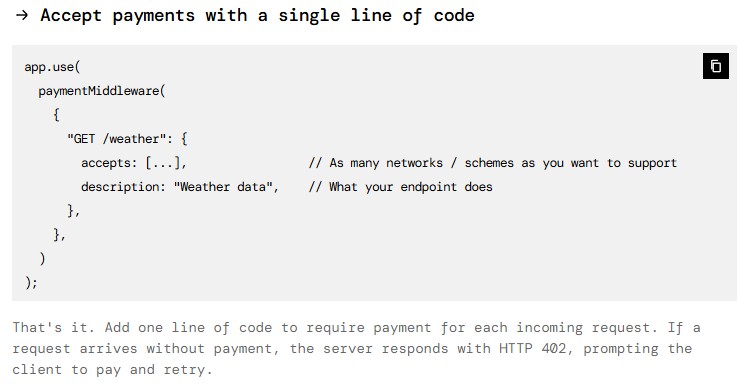

Critically, it does this with a simple line of code.

Source: https://www.x402.org/

Instead of creating accounts, entering card details and subscribing to services, a client – human or machine – can simply respond to an HTTP request that says: “Payment required.”

This transforms payments from a separate process into a built-in feature of the internet itself.

Why does this matter?

Because the next economy will include autonomous economic actors. Imagine:

- AI models paying for data in real time

- IoT devices paying for electricity or bandwidth

- algorithms purchasing compute power on demand

- AI agents negotiating and settling micro-transactions across networks

Traditional payment rails were never designed for this environment. They rely on accounts, credentials, onboarding processes and manual approval flows – all friction points that slow down machine-speed commerce. Internet-native payment protocols remove that friction and unlock new capabilities:

- micropayments at scale – fractions of a cent for data or content

- machine-to-machine commerce

- instant settlement

- programmable value exchange

In short, they allow value to move at the speed of the internet, and the implications go far beyond faster payments. If every API endpoint or web service can request payment directly, then every digital interaction becomes a potential commercial transaction. This moves us from basic embedded payments to a place where pricing, settlement and financial logic are embedded directly into digital infrastructure.

It’s invisible finance.

Businesses could charge per API call, per data request or per algorithm execution. Revenue shifts from subscription billing to consumption-based monetisation, aligning cost with actual usage.

The thing is that this transformation of payments is not happening in isolation. It sits at the intersection of several major technology shifts, including:

- tokenised deposits and digital currencies

- stablecoins

- programmable payments

- agentic AI

- on-chain digital identity for machines

- AI-driven fraud detection

Together, these innovations create the foundations for a programmable financial system where value flows automatically between humans, machines and platforms.

It also raises a lot of new governance questions.

- if an AI initiates a payment, who is accountable?

- how do regulators monitor real-time machine transactions?

- how do AML and fraud frameworks adapt to autonomous systems?

Just as open banking triggered new regulatory frameworks such as PSD2, the next era of payments will require updated rules for AI-driven financial activity.

What does this mean for traditional financial institutions?

I think the message is clear. The payments ecosystem is shifting from human-initiated transactions to machine-initiated value flows. Banks and payment providers must therefore rethink their architecture to support:

- multi-asset payments (fiat, stablecoins, digital currencies)

- real-time programmable settlement

- AI-initiated transactions

- interoperable digital identity systems

Those that adapt early will be positioned to capture the emerging machine economy. Those that don’t may find that payments – the lifeblood of finance – increasingly happen outside the traditional banking stack.

Chris M Skinner

Chris Skinner is best known as an independent commentator on the financial markets through his blog, TheFinanser.com, as author of the bestselling book Digital Bank, and Chair of the European networking forum the Financial Services Club. He has been voted one of the most influential people in banking by The Financial Brand (as well as one of the best blogs), a FinTech Titan (Next Bank), one of the Fintech Leaders you need to follow (City AM, Deluxe and Jax Finance), as well as one of the Top 40 most influential people in financial technology by the Wall Street Journal's Financial News. To learn more click here...