I remember making a prediction twenty-five years ago that all of the biggest banks in the world would be Chinese. Unfortunately, I made this prediction at an American banking conference, when all of the biggest banks in the world were American. Twenty-five years earlier, or fifty years ago, all of the biggest banks were Japanese.

The world pivots regularly in finance.

This is typified by the 2008 financial crisis when Jamie Dimon’s daughter asked him: “What’s a financial crisis?” and his answer was something that happens around every seven years.

In other words, you think the world is strong and stable, but it’s not. It changes every day and the financial base of the world demonstrates how power and concentration moves from one base to another.

Notably, European banks have never ridden high in the bank asset charts for the past fifty years. There have been moments, but the likes of HSBC and other EU banks have never reached the heights of JP Morgan Chase or Industrial and Commercial Bank of China (ICBC).

Why?

It’s actually very simple: HSBC built a network; JPMorgan built a machine; whilst ICBC built a system; and, in today’s financial markets, machines and systems will always be worth more than networks.

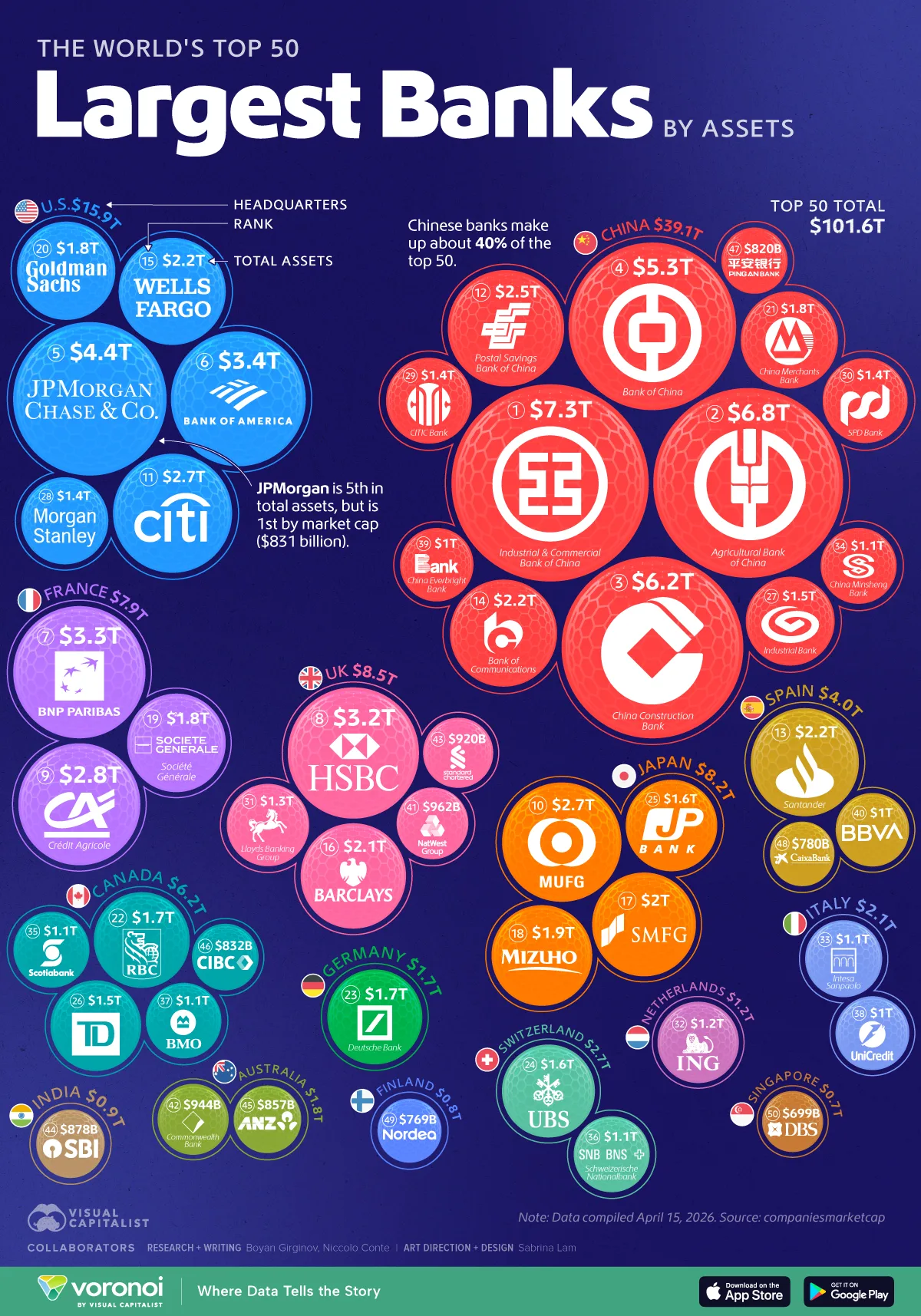

Source: Ranked: The World’s 50 Largest Banks by Assets

Let’s talk about it and start with a simple question: why has HSBC – arguably the most international bank on the planet – never been worth more than JPMorgan Chase or ICBC?

At first glance, it doesn’t make sense. HSBC has the history, the global footprint, the brand. It was THE bank that connected East and West. If banking was just about geography, HSBC should win hands down, but banking isn’t about geography. It’s about returns and this is where the story gets interesting as it is the network versus the machine.

HSBC built a network. A beautiful, sprawling, complex network that stretches across continents. The problem is that networks are hard to manage as there are different regulators, different political systems, different currencies and different risks. Every country adds friction, cost and uncertainty. What looks like diversification on a PowerPoint slide often turns into dilution in a balance sheet.

Compare that with JPMorgan Chase.

Under Jamie Dimon, JPMorgan didn’t try to be everything everywhere. It built a machine. A highly efficient, highly focused, deeply integrated machine anchored in the most profitable banking market in the world: the United States and yes, it is global, but it expands from strength, not from ambition and markets love machines. They are predictable. They generate consistent returns. They scale.

Then there’s Industrial and Commercial Bank of China, which plays a completely different game. ICBC isn’t just a bank competing in a market. It is part of a system – the Chinese economic system. That means scale at a level Western banks struggle to comprehend because the Chinese system is based upon access to low-cost funding and an implicit alignment with national growth. When China grows, ICBC grows. It’s that simple.

Investors understand that story. It’s big, it’s directional, and it’s backed by a system …

… and this is HSBC’s real problem. It sits between two worlds. Too global to be focused like JPMorgan and too market-driven to be supported like ICBC. This is why, for the past two decades, HSBC has spent more time reshaping itself than executing a clear strategy.

Global bank. Asian bank. Exit markets. Re-enter markets. Pivot. Restructure. Repeat.

Investors don’t pay a premium for “we’re still figuring it out”. They discount it.

In other words, the problem with HSBC is too many moving parts, too many jurisdictions and too many unknowns. It’s hard to model, hard to predict, and therefore hard to value at a premium. Meanwhile, JPMorgan delivers consistent returns quarter after quarter and ICBC rides the momentum of the Chinese economy. Both have clear narratives whilst HSBC has complexity.

Chris M Skinner

Chris Skinner is best known as an independent commentator on the financial markets through his blog, TheFinanser.com, as author of the bestselling book Digital Bank, and Chair of the European networking forum the Financial Services Club. He has been voted one of the most influential people in banking by The Financial Brand (as well as one of the best blogs), a FinTech Titan (Next Bank), one of the Fintech Leaders you need to follow (City AM, Deluxe and Jax Finance), as well as one of the Top 40 most influential people in financial technology by the Wall Street Journal's Financial News. To learn more click here...