Thirty years ago, I wrote a strategy report for NCR, where I was working at the time, saying that the future of banking would be branchless and cashless, which was not great news for a company selling cash machines.

Now, we live in a world that is nearing branchless and cashless. I’ve written quite a lot about branch closures and the issues around that theme:

Why bank branches still matter (part one)

Human needs for human service (why branches matter, part two)

Branches aren’t needed for advice or transactions … it’s all about trust

The thing is that my prediction in the 1990s was that we needed about a tenth of the branch network that we had back then. Most banks had over 1,000 branches. They only need 100, but I never said we would never need branches.

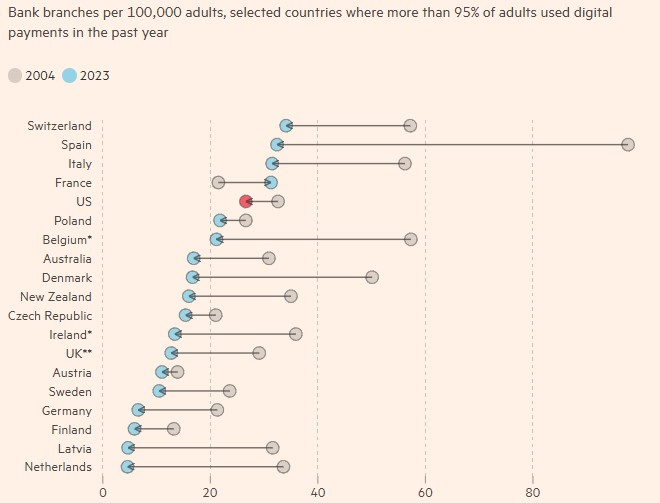

Nevertheless, banks are moving rapidly away from physical distribution and want customers to use digital services. Over the past decade alone in the UK, more than 6,600 bank and building society branches have closed, a loss of more than two-thirds of the network with closures averaging over 50 branches per month.

Source: The Financial Times

Interestingly, customers don’t like it, as illustrated by two articles the other day:

High-street banks should think again about cutting in-person services

Equally, the use of paper in banking has been something we have tried to eradicate for years. The card companies Visa and MasterCard have had a war on cash for over twenty years, and the UK Government decided in 2012 to ban the use of paper cheques for payments. Well, they both failed as we still use cheques and cash.

The last figures I picked up are that cheque usage has declined significantly in the last decade, but people still use them. According to stats from UK Finance, Brits banked 91 million cheques in 2024. The same with cash. Usage has declined, but we still like cash.

LINK, which runs the UK’s ATM network, ran a survey of 1,116 high street SMEs in September 2025 to assess cash acceptance and payment habits, and found that cash is maybe not King but it’s still relevant.

You can download the report here but here’s a quick summary:

Cash is declining but still widely used

Cash use in the UK is falling rapidly as consumers increasingly use cards, phones, and digital payments. Cash now represents less than 10% of total payments, and ATM withdrawals on the LINK network have fallen significantly since 2018.

However, cash remains important for many people—especially those who are financially vulnerable, digitally excluded, or using cash for budgeting.

Most high-street businesses still accept cash

The survey of 1,116 UK SMEs found that:

- 77% of high-street businesses still accept cash

- 46% of in-person transactions are cash

- 55% of businesses actively encourage cash payments

- 14% of retailers went cashless in the past year

Cash acceptance varies by location:

- Urban areas: ~80% accept cash

- Suburban/coastal areas: ~72% accept cash

Why businesses are going cashless

Retailers are not abandoning cash purely because of falling demand. The main drivers are operational pressures:

Top reasons businesses stop accepting cash

- Fraud risks (counterfeit notes)

- Security concerns and theft risk

- Declining customer demand

- Cash-handling costs (deposit fees, insurance, transport)

- Easier bookkeeping with digital payments

Bank branch closures and limited deposit facilities also make handling cash harder for businesses.

Cash still offers real advantages

Despite the shift to digital payments, cash continues to provide important benefits for retailers and consumers:

- Avoids card processing fees

- Immediate liquidity for small businesses

- Faster small transactions

- Works during internet or system outages

- Supports financially vulnerable customers

For these reasons, many retailers believe cash supports inclusion and resilience on the high street.

Cash acceptance is expected to keep falling

The research suggests the decline will continue:

- 56% of retailers say cash usage has fallen in the past two years

- 55% expect further decline

- 4% plan to stop accepting cash within two years

More than half of businesses (51%) believe declining cash acceptance harms the high street, reducing accessibility and customer inclusion.

Key risks identified

The report warns that without intervention the UK could develop a “two-tier payment society”, where people who cannot use digital payments struggle to participate in everyday commerce.

This would affect groups such as:

- Low-income households

- Elderly people

- Digitally excluded individuals

- Victims of financial control or abuse

Recommendations from the report

To preserve payment choice, the report recommends:

- Strengthen cash deposit infrastructure (banking hubs, Post Offices, deposit ATMs).

- Tackle retail crime and fraud to reduce security risks linked to cash handling.

- Monitor cash acceptance (not just access to cash withdrawals).

- Promote a balanced payments ecosystem where both digital payments and cash coexist.

The bottom line is that cash is declining but remains economically and socially important. While most businesses still accept it, rising costs, security risks, and shrinking banking infrastructure are pushing retailers toward cashless models. So yes, we are now becoming branchless and cashless whether we like it or not.

Postnote: total aside but the UK is ending its analogue telephone system from January 1 2027. It's digital only.

Chris M Skinner

Chris Skinner is best known as an independent commentator on the financial markets through his blog, TheFinanser.com, as author of the bestselling book Digital Bank, and Chair of the European networking forum the Financial Services Club. He has been voted one of the most influential people in banking by The Financial Brand (as well as one of the best blogs), a FinTech Titan (Next Bank), one of the Fintech Leaders you need to follow (City AM, Deluxe and Jax Finance), as well as one of the Top 40 most influential people in financial technology by the Wall Street Journal's Financial News. To learn more click here...